by

Garrett Clark

Investment Guidance

Can Your Solo 401(k) Invest in Startups?

Curious about investing in startups through your retirement account? A self-directed Solo 401(k) may provide access to private companies, startup ventures, and other alternative investments beyond traditional stocks and mutual funds. In this article, we explore how startup investing works within a Solo 401(k), the potential benefits and risks, important IRS rules to understand, and key considerations before investing retirement funds in private businesses. Learn how entrepreneurs and self-directed investors are using Solo 401(k)s to pursue diversification, greater investment control, and long-term wealth-building opportunities.

Search

Search

Category

Any Question?

Let’s talk

Any Question?

Let’s talk

Search

Search

Category

Any Question?

Let’s talk

For many investors, some of the greatest wealth-building opportunities have come from owning shares in private companies before they became household names. Companies like Amazon, Tesla, Uber, Airbnb, and countless others created substantial returns for early investors who recognized their potential before they went public.

As interest in private investing continues to grow, many self-directed retirement investors are asking an important question:

Can a Solo 401(k) invest in startups?

The answer is often yes, provided the investment complies with IRS rules, plan documents, and applicable regulations.

For entrepreneurs, accredited investors, angel investors, and those seeking opportunities beyond traditional stocks and mutual funds, startup investing inside a Solo 401(k) can be an intriguing strategy. However, it is important to understand both the opportunities and the responsibilities involved.

Let's take a closer look.

Understanding Self-Directed Solo 401(k) Investing

Many traditional retirement plans limit participants to investments such as:

Mutual funds

ETFs

Stocks

Bonds

Target-date funds

While these investments can play an important role in a retirement portfolio, some investors prefer access to a broader range of opportunities.

A properly structured self-directed Solo 401(k) may provide access to alternative investments, including:

Real estate

Private lending

Precious metals

Tax liens

Private placements

Limited partnerships

Certain startup investments

This flexibility is one reason many entrepreneurs and sophisticated investors choose self-directed retirement plans.

What Is Considered a Startup Investment?

A startup investment generally involves purchasing an ownership interest in a private company that is in its early stages of growth.

Examples may include:

Technology startups

Software companies

Healthcare ventures

Manufacturing businesses

E-commerce companies

Artificial intelligence businesses

Consumer product companies

Service-based startups

Rather than purchasing shares on a public stock exchange, investors typically acquire ownership through private offerings.

These investments often occur during:

Seed rounds

Angel investment rounds

Series A funding rounds

Private placements

Because these companies are not publicly traded, investors may gain exposure to growth opportunities that are unavailable through traditional brokerage accounts.

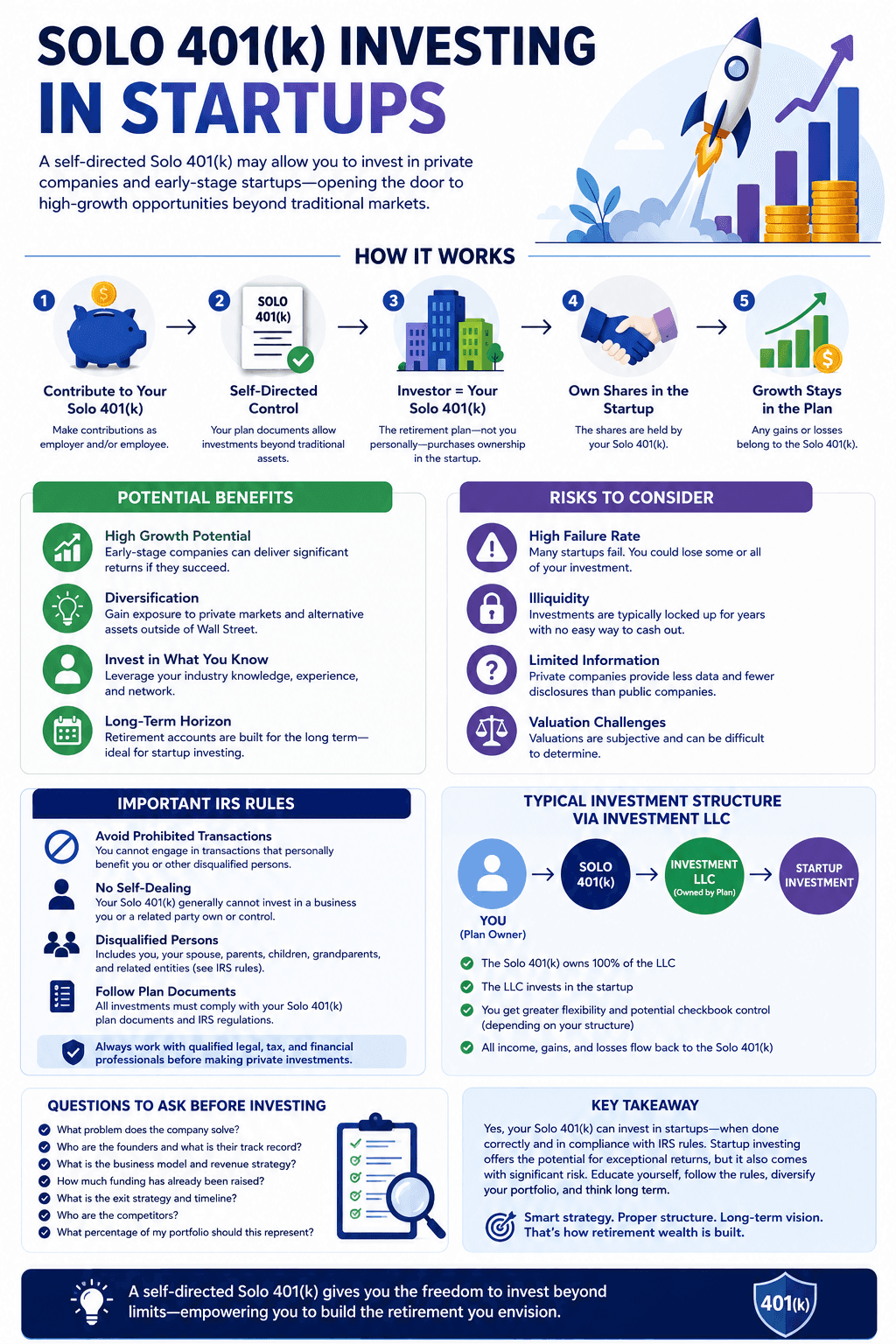

How a Solo 401(k) Can Invest in a Startup

When investing through a Solo 401(k), the retirement plan—not you personally—is the investor.

For example, if your Solo 401(k) purchases ownership in a startup company:

The shares are owned by the Solo 401(k)

Any gains belong to the Solo 401(k)

Any losses impact the Solo 401(k)

Investment proceeds flow back into the retirement plan

The investment remains separate from your personal assets.

This separation is one of the most important principles of self-directed retirement investing.

Why Some Investors Use Retirement Funds for Startup Investments

Startup investing carries significant risk, but some investors are attracted to the potential advantages.

Access to High Growth Opportunities

Public markets often represent companies that have already experienced substantial growth.

By investing earlier in a company's lifecycle, investors may gain exposure to growth before a public offering or acquisition occurs.

Diversification

Many retirement portfolios are heavily concentrated in public securities.

Startup investing can provide exposure to private markets and alternative asset classes.

Alignment With Personal Expertise

Some investors work in industries where they possess specialized knowledge.

An entrepreneur with experience in software, healthcare, construction, or manufacturing may feel more comfortable evaluating opportunities within their field.

Long-Term Investment Horizon

Retirement accounts are generally designed for long-term investing.

Because startup investments often require years to mature, some investors view retirement accounts as a natural place to hold these investments.

Understanding the Risks

While startup investing can be exciting, it is important to understand the risks involved.

High Failure Rates

Most startups do not become billion-dollar success stories.

In fact, many fail.

Investors should be prepared for the possibility of losing some or all of their investment.

Illiquidity

Unlike publicly traded stocks, startup investments often cannot be easily sold.

You may need to hold the investment for years before an exit event occurs.

Limited Information

Private companies generally provide less information than publicly traded corporations.

Investors often have fewer disclosures and less historical data available.

Valuation Challenges

Determining the true value of a startup can be difficult.

Without public market pricing, valuations may be subjective.

Regulatory Complexity

Private investments often involve securities regulations, subscription agreements, and investment documentation that require careful review.

Important IRS Rules to Understand

Although a Solo 401(k) can often invest in startups, there are important restrictions that must be followed.

Prohibited Transactions

The IRS prohibits certain transactions between a retirement plan and disqualified persons.

Generally, you cannot use retirement funds in a manner that personally benefits you outside the retirement plan.

Self-Dealing Concerns

One of the most common mistakes investors make is attempting to use retirement funds to benefit businesses they personally control.

For example, if you own a startup personally, your Solo 401(k) generally cannot simply invest in your own company.

These situations can create prohibited transaction concerns.

Disqualified Persons

Certain individuals have special restrictions when interacting with retirement plan assets.

These may include:

The account owner

Spouses

Parents

Grandparents

Children

Certain business entities

Because these rules can be complex, investors should seek qualified legal and tax guidance before making private investments.

Startup Investing Through a Solo 401(k) LLC

Some investors establish a Solo 401(k) structure that includes an investment LLC owned by the retirement plan.

In these situations:

Solo 401(k)

↓

Investment LLC

↓

Startup Investment

This structure may provide greater investment flexibility and checkbook control, depending on the circumstances.

Many investors utilize this type of structure when making alternative investments that require timely transactions.

Questions to Ask Before Investing

Before investing retirement funds into a startup, consider asking:

What problem does the company solve?

Who are the founders?

What is the revenue model?

How much capital has already been raised?

What is the exit strategy?

Who are the competitors?

How long might the investment be held?

What percentage of my portfolio should be allocated to this investment?

Due diligence becomes even more important when investing in private companies.

Startup Investing and Long-Term Wealth Building

Startup investing should generally be viewed as one component of a diversified retirement strategy.

Many investors choose to balance startup investments with:

Public stocks

ETFs

Real estate

Private lending

Precious metals

Cash reserves

Diversification can help manage risk while maintaining exposure to potential growth opportunities.

The goal is not necessarily finding the next billion-dollar company.

The goal is building a retirement portfolio aligned with your risk tolerance, investment objectives, and long-term financial plan.

Final Thoughts

So, can your Solo 401(k) invest in startups?

In many cases, yes.

A properly structured self-directed Solo 401(k) may allow investments in private companies, startup ventures, and other alternative assets that are unavailable through many traditional retirement accounts.

However, startup investing involves substantial risk, complex regulations, and important IRS rules that must be followed carefully. Investors should conduct thorough due diligence and consult qualified legal, tax, and financial professionals before making investment decisions.

For those who understand the risks and opportunities, startup investing can be another example of how a self-directed Solo 401(k) may provide greater flexibility and control over retirement assets.

At Survival401k, we help entrepreneurs and investors understand the opportunities available through self-directed Solo 401(k) plans, including alternative investments, checkbook control structures, and retirement strategies designed to put you in the driver's seat of your financial future.

This article is for educational purposes only and should not be considered tax, legal, financial, or investment advice.

For many investors, some of the greatest wealth-building opportunities have come from owning shares in private companies before they became household names. Companies like Amazon, Tesla, Uber, Airbnb, and countless others created substantial returns for early investors who recognized their potential before they went public.

As interest in private investing continues to grow, many self-directed retirement investors are asking an important question:

Can a Solo 401(k) invest in startups?

The answer is often yes, provided the investment complies with IRS rules, plan documents, and applicable regulations.

For entrepreneurs, accredited investors, angel investors, and those seeking opportunities beyond traditional stocks and mutual funds, startup investing inside a Solo 401(k) can be an intriguing strategy. However, it is important to understand both the opportunities and the responsibilities involved.

Let's take a closer look.

Understanding Self-Directed Solo 401(k) Investing

Many traditional retirement plans limit participants to investments such as:

Mutual funds

ETFs

Stocks

Bonds

Target-date funds

While these investments can play an important role in a retirement portfolio, some investors prefer access to a broader range of opportunities.

A properly structured self-directed Solo 401(k) may provide access to alternative investments, including:

Real estate

Private lending

Precious metals

Tax liens

Private placements

Limited partnerships

Certain startup investments

This flexibility is one reason many entrepreneurs and sophisticated investors choose self-directed retirement plans.

What Is Considered a Startup Investment?

A startup investment generally involves purchasing an ownership interest in a private company that is in its early stages of growth.

Examples may include:

Technology startups

Software companies

Healthcare ventures

Manufacturing businesses

E-commerce companies

Artificial intelligence businesses

Consumer product companies

Service-based startups

Rather than purchasing shares on a public stock exchange, investors typically acquire ownership through private offerings.

These investments often occur during:

Seed rounds

Angel investment rounds

Series A funding rounds

Private placements

Because these companies are not publicly traded, investors may gain exposure to growth opportunities that are unavailable through traditional brokerage accounts.

How a Solo 401(k) Can Invest in a Startup

When investing through a Solo 401(k), the retirement plan—not you personally—is the investor.

For example, if your Solo 401(k) purchases ownership in a startup company:

The shares are owned by the Solo 401(k)

Any gains belong to the Solo 401(k)

Any losses impact the Solo 401(k)

Investment proceeds flow back into the retirement plan

The investment remains separate from your personal assets.

This separation is one of the most important principles of self-directed retirement investing.

Why Some Investors Use Retirement Funds for Startup Investments

Startup investing carries significant risk, but some investors are attracted to the potential advantages.

Access to High Growth Opportunities

Public markets often represent companies that have already experienced substantial growth.

By investing earlier in a company's lifecycle, investors may gain exposure to growth before a public offering or acquisition occurs.

Diversification

Many retirement portfolios are heavily concentrated in public securities.

Startup investing can provide exposure to private markets and alternative asset classes.

Alignment With Personal Expertise

Some investors work in industries where they possess specialized knowledge.

An entrepreneur with experience in software, healthcare, construction, or manufacturing may feel more comfortable evaluating opportunities within their field.

Long-Term Investment Horizon

Retirement accounts are generally designed for long-term investing.

Because startup investments often require years to mature, some investors view retirement accounts as a natural place to hold these investments.

Understanding the Risks

While startup investing can be exciting, it is important to understand the risks involved.

High Failure Rates

Most startups do not become billion-dollar success stories.

In fact, many fail.

Investors should be prepared for the possibility of losing some or all of their investment.

Illiquidity

Unlike publicly traded stocks, startup investments often cannot be easily sold.

You may need to hold the investment for years before an exit event occurs.

Limited Information

Private companies generally provide less information than publicly traded corporations.

Investors often have fewer disclosures and less historical data available.

Valuation Challenges

Determining the true value of a startup can be difficult.

Without public market pricing, valuations may be subjective.

Regulatory Complexity

Private investments often involve securities regulations, subscription agreements, and investment documentation that require careful review.

Important IRS Rules to Understand

Although a Solo 401(k) can often invest in startups, there are important restrictions that must be followed.

Prohibited Transactions

The IRS prohibits certain transactions between a retirement plan and disqualified persons.

Generally, you cannot use retirement funds in a manner that personally benefits you outside the retirement plan.

Self-Dealing Concerns

One of the most common mistakes investors make is attempting to use retirement funds to benefit businesses they personally control.

For example, if you own a startup personally, your Solo 401(k) generally cannot simply invest in your own company.

These situations can create prohibited transaction concerns.

Disqualified Persons

Certain individuals have special restrictions when interacting with retirement plan assets.

These may include:

The account owner

Spouses

Parents

Grandparents

Children

Certain business entities

Because these rules can be complex, investors should seek qualified legal and tax guidance before making private investments.

Startup Investing Through a Solo 401(k) LLC

Some investors establish a Solo 401(k) structure that includes an investment LLC owned by the retirement plan.

In these situations:

Solo 401(k)

↓

Investment LLC

↓

Startup Investment

This structure may provide greater investment flexibility and checkbook control, depending on the circumstances.

Many investors utilize this type of structure when making alternative investments that require timely transactions.

Questions to Ask Before Investing

Before investing retirement funds into a startup, consider asking:

What problem does the company solve?

Who are the founders?

What is the revenue model?

How much capital has already been raised?

What is the exit strategy?

Who are the competitors?

How long might the investment be held?

What percentage of my portfolio should be allocated to this investment?

Due diligence becomes even more important when investing in private companies.

Startup Investing and Long-Term Wealth Building

Startup investing should generally be viewed as one component of a diversified retirement strategy.

Many investors choose to balance startup investments with:

Public stocks

ETFs

Real estate

Private lending

Precious metals

Cash reserves

Diversification can help manage risk while maintaining exposure to potential growth opportunities.

The goal is not necessarily finding the next billion-dollar company.

The goal is building a retirement portfolio aligned with your risk tolerance, investment objectives, and long-term financial plan.

Final Thoughts

So, can your Solo 401(k) invest in startups?

In many cases, yes.

A properly structured self-directed Solo 401(k) may allow investments in private companies, startup ventures, and other alternative assets that are unavailable through many traditional retirement accounts.

However, startup investing involves substantial risk, complex regulations, and important IRS rules that must be followed carefully. Investors should conduct thorough due diligence and consult qualified legal, tax, and financial professionals before making investment decisions.

For those who understand the risks and opportunities, startup investing can be another example of how a self-directed Solo 401(k) may provide greater flexibility and control over retirement assets.

At Survival401k, we help entrepreneurs and investors understand the opportunities available through self-directed Solo 401(k) plans, including alternative investments, checkbook control structures, and retirement strategies designed to put you in the driver's seat of your financial future.

This article is for educational purposes only and should not be considered tax, legal, financial, or investment advice.