by

Garrett Clark

Retirement Planning

How Fitness Professionals on 1099 Income Can Use an LLC and Solo 401(k) to Build Wealth and Their Business

Fitness professionals earning 1099 income have a unique opportunity to build real wealth. This guide breaks down how to use an LLC and Solo 401(k) together to reduce taxes, access capital, and create long-term financial growth through smarter structure and strategy.

Search

Search

Category

Any Question?

Let’s talk

Any Question?

Let’s talk

Search

Search

Category

Any Question?

Let’s talk

Fitness professionals operate in one of the most opportunity-rich financial positions today. Whether you are a personal trainer, gym owner, online coach, or fitness influencer, earning 1099 income gives you something most employees never have: control.

No employer plan. No automatic structure. No built-in system.

While that can feel uncertain, it actually creates a powerful advantage. With the right setup, you can build a system that not only grows your business but also compounds wealth over time.

By combining an LLC with a Solo 401(k), fitness professionals can create a framework that reduces taxes, increases flexibility, and opens doors to advanced wealth-building strategies most people never access.

Step One: Structure Your Income With an LLC

An LLC is the foundation of your financial system. Without structure, income is just income. With an LLC, income becomes strategic.

When you operate under an LLC, you separate personal and business finances, which protects your assets and creates a clean, professional structure for growth.

Why This Matters

Fitness professionals often juggle multiple income streams:

In-person training

Online coaching programs

Brand deals and sponsorships

Affiliate income

Digital products and courses

Without structure, this becomes messy. With an LLC, it becomes scalable.

Advanced Wealth Uses of an LLC

An LLC is not just for an organization; it is a tool for building wealth:

Deduct and reinvest: Write off legitimate expenses and reinvest the savings back into your business

Control cash flow: Keep earnings inside the business to strategically deploy capital

Expand into new ventures: Launch additional income streams under one entity

Position for S-Corp election: Reduce self-employment taxes as income grows

The LLC is where money is earned and optimized.

Step Two: Use a Solo 401(k) as a Wealth Engine

A Solo 401(k) takes what your LLC generates and turns it into long-term wealth.

Most people think of retirement accounts as restrictive. A properly structured Solo 401(k) is the opposite. It gives you control, flexibility, and scale.

Dual Contribution Advantage

You can contribute as:

The employee

The employer

This allows you to significantly reduce taxable income while moving large amounts of money into a tax-advantaged environment.

“Most fitness professionals focus on making more money. The ones who build wealth focus on structuring it.”

Garrett Clark

Director of Sales

Investment Control

Unlike traditional plans, a Solo 401(k) allows you to direct how your money is invested.

Depending on the structure, this can include:

Stocks and ETFs

Real estate

Private lending

Alternative investments

This turns your retirement account into a growth vehicle, not just a savings account.

Step Three: Use Leverage and Capital Strategically

This is where most people miss the opportunity.

A Solo 401(k) is not just for saving; it can also be used to access capital strategically.

The Solo 401(k) Loan Feature

A properly structured Solo 401(k) may allow you to borrow from your own plan within IRS limits.

This creates a powerful advantage:

You access capital without relying on banks

You repay yourself with interest

Your money continues working within your system

Strategic Uses of the Loan Feature

For fitness professionals, this can be used to:

Open or expand a gym or studio

Invest in high-quality equipment

Launch or scale an online coaching platform

Fund marketing and brand growth

Bridge short-term cash flow gaps

Instead of seeking outside funding, you may be able to be your own lender.

Private Lending Inside a Solo 401(k)

Another advanced strategy is using your Solo 401(k) to lend money to third parties (not yourself or disqualified persons).

This allows you to:

Earn interest inside your retirement account

Generate passive income

Build consistent returns independent of your business

Real Estate and Alternative Investing

With the right structure, your Solo 401(k) can invest in:

Rental properties

Real estate deals

Private placements

This creates diversification beyond your fitness income and allows your retirement account to grow from multiple sources.

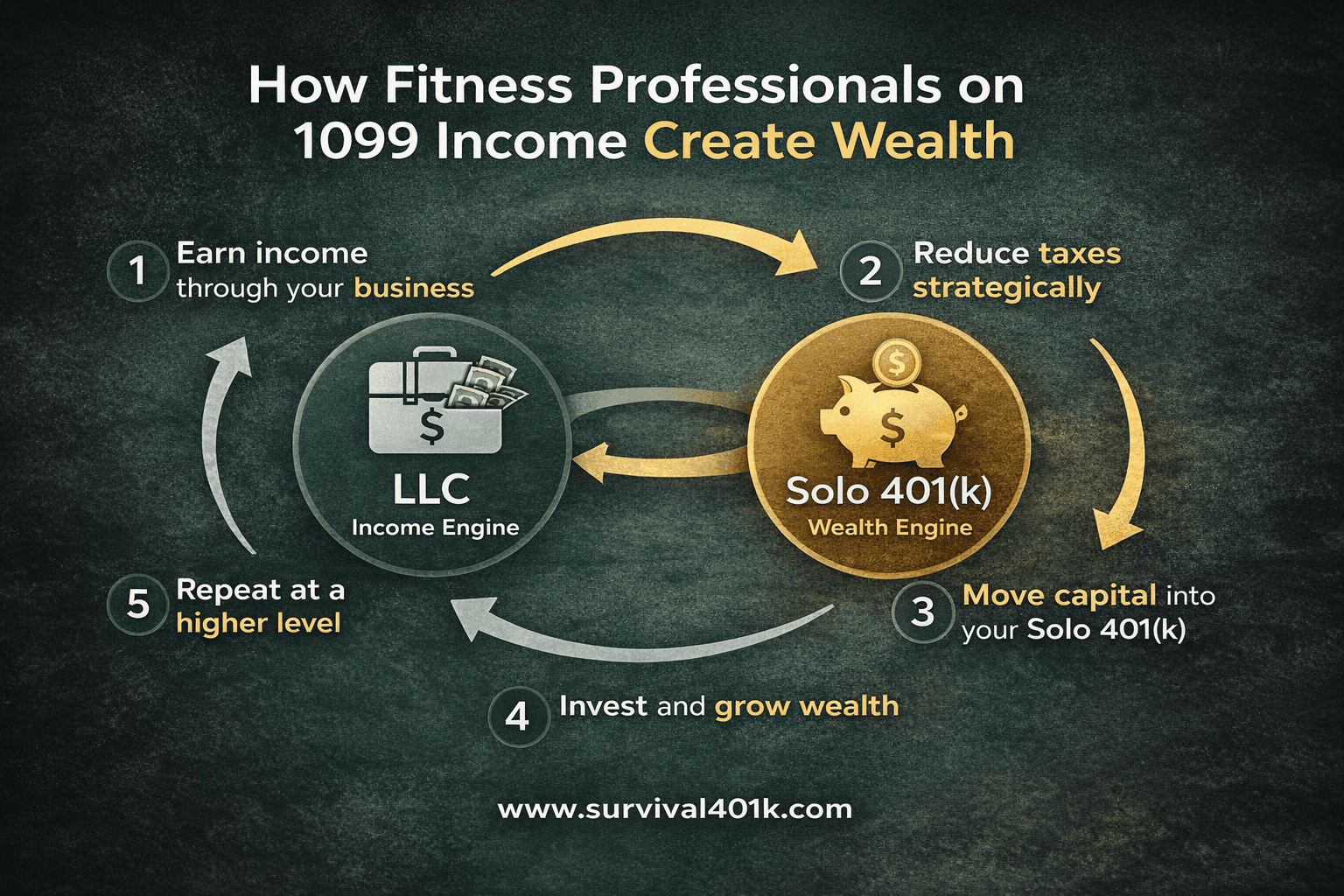

How the LLC and Solo 401(k) Work Together

This is where the real power comes in.

Think of it as a system:

LLC = Income Engine

Solo 401(k) = Wealth Engine

Your LLC:

Generates income

Reduces taxes through deductions

Creates cash flow

Your Solo 401(k):

Captures that income

Protects it from taxes

Grows it through investments

Together, they create a loop:

Earn income through your business

Reduce taxes strategically

Move capital into your Solo 401(k)

Invest and grow wealth

Repeat at a higher level

Building Today While Preparing for Tomorrow

The fitness industry is physically demanding and often unpredictable. Income can peak early, fluctuate, or depend heavily on personal branding.

That is why structure matters.

When you build systems early:

You are not relying on your body forever

You are not dependent on an inconsistent income

You are building assets alongside your business

What This Strategy Actually Does

Reduces unnecessary taxes

Protects your income and assets

Creates access to capital when needed

Builds long-term, compounding wealth

Most fitness professionals focus only on earning more.

The real advantage comes from keeping more and growing it correctly.

The Bigger Picture

For 1099 fitness professionals, the goal is not just income. It is control.

When structured correctly:

Your business funds your lifestyle

Your tax strategy preserves your income

Your investments build your future

Retirement becomes the outcome.

Control is the strategy.

Next Steps

If you are earning 1099 income and want to:

Lower your tax burden

Structure your business correctly

Access more financial opportunities

Build long-term wealth

It starts with putting the right system in place.

This content is for educational purposes only and should not be considered legal, tax, or investment advice. Every individual situation is different, and strategies discussed may not be appropriate for all readers.

Fitness professionals operate in one of the most opportunity-rich financial positions today. Whether you are a personal trainer, gym owner, online coach, or fitness influencer, earning 1099 income gives you something most employees never have: control.

No employer plan. No automatic structure. No built-in system.

While that can feel uncertain, it actually creates a powerful advantage. With the right setup, you can build a system that not only grows your business but also compounds wealth over time.

By combining an LLC with a Solo 401(k), fitness professionals can create a framework that reduces taxes, increases flexibility, and opens doors to advanced wealth-building strategies most people never access.

Step One: Structure Your Income With an LLC

An LLC is the foundation of your financial system. Without structure, income is just income. With an LLC, income becomes strategic.

When you operate under an LLC, you separate personal and business finances, which protects your assets and creates a clean, professional structure for growth.

Why This Matters

Fitness professionals often juggle multiple income streams:

In-person training

Online coaching programs

Brand deals and sponsorships

Affiliate income

Digital products and courses

Without structure, this becomes messy. With an LLC, it becomes scalable.

Advanced Wealth Uses of an LLC

An LLC is not just for an organization; it is a tool for building wealth:

Deduct and reinvest: Write off legitimate expenses and reinvest the savings back into your business

Control cash flow: Keep earnings inside the business to strategically deploy capital

Expand into new ventures: Launch additional income streams under one entity

Position for S-Corp election: Reduce self-employment taxes as income grows

The LLC is where money is earned and optimized.

Step Two: Use a Solo 401(k) as a Wealth Engine

A Solo 401(k) takes what your LLC generates and turns it into long-term wealth.

Most people think of retirement accounts as restrictive. A properly structured Solo 401(k) is the opposite. It gives you control, flexibility, and scale.

Dual Contribution Advantage

You can contribute as:

The employee

The employer

This allows you to significantly reduce taxable income while moving large amounts of money into a tax-advantaged environment.

“Most fitness professionals focus on making more money. The ones who build wealth focus on structuring it.”

Garrett Clark

Director of Sales

Investment Control

Unlike traditional plans, a Solo 401(k) allows you to direct how your money is invested.

Depending on the structure, this can include:

Stocks and ETFs

Real estate

Private lending

Alternative investments

This turns your retirement account into a growth vehicle, not just a savings account.

Step Three: Use Leverage and Capital Strategically

This is where most people miss the opportunity.

A Solo 401(k) is not just for saving; it can also be used to access capital strategically.

The Solo 401(k) Loan Feature

A properly structured Solo 401(k) may allow you to borrow from your own plan within IRS limits.

This creates a powerful advantage:

You access capital without relying on banks

You repay yourself with interest

Your money continues working within your system

Strategic Uses of the Loan Feature

For fitness professionals, this can be used to:

Open or expand a gym or studio

Invest in high-quality equipment

Launch or scale an online coaching platform

Fund marketing and brand growth

Bridge short-term cash flow gaps

Instead of seeking outside funding, you may be able to be your own lender.

Private Lending Inside a Solo 401(k)

Another advanced strategy is using your Solo 401(k) to lend money to third parties (not yourself or disqualified persons).

This allows you to:

Earn interest inside your retirement account

Generate passive income

Build consistent returns independent of your business

Real Estate and Alternative Investing

With the right structure, your Solo 401(k) can invest in:

Rental properties

Real estate deals

Private placements

This creates diversification beyond your fitness income and allows your retirement account to grow from multiple sources.

How the LLC and Solo 401(k) Work Together

This is where the real power comes in.

Think of it as a system:

LLC = Income Engine

Solo 401(k) = Wealth Engine

Your LLC:

Generates income

Reduces taxes through deductions

Creates cash flow

Your Solo 401(k):

Captures that income

Protects it from taxes

Grows it through investments

Together, they create a loop:

Earn income through your business

Reduce taxes strategically

Move capital into your Solo 401(k)

Invest and grow wealth

Repeat at a higher level

Building Today While Preparing for Tomorrow

The fitness industry is physically demanding and often unpredictable. Income can peak early, fluctuate, or depend heavily on personal branding.

That is why structure matters.

When you build systems early:

You are not relying on your body forever

You are not dependent on an inconsistent income

You are building assets alongside your business

What This Strategy Actually Does

Reduces unnecessary taxes

Protects your income and assets

Creates access to capital when needed

Builds long-term, compounding wealth

Most fitness professionals focus only on earning more.

The real advantage comes from keeping more and growing it correctly.

The Bigger Picture

For 1099 fitness professionals, the goal is not just income. It is control.

When structured correctly:

Your business funds your lifestyle

Your tax strategy preserves your income

Your investments build your future

Retirement becomes the outcome.

Control is the strategy.

Next Steps

If you are earning 1099 income and want to:

Lower your tax burden

Structure your business correctly

Access more financial opportunities

Build long-term wealth

It starts with putting the right system in place.

This content is for educational purposes only and should not be considered legal, tax, or investment advice. Every individual situation is different, and strategies discussed may not be appropriate for all readers.