by

Garrett Clark

Investment Guidance

Non-Recourse Lending in Self-Directed Accounts

Learn how non-recourse lending works inside a Solo 401(k) or Self-Directed IRA and how it can help you scale real estate investments without personal liability. This guide breaks down the structure, tax advantages, key rules, and when this strategy makes sense so you can make informed investment decisions.

Search

Search

Category

Any Question?

Let’s talk

Any Question?

Let’s talk

Search

Search

Category

Any Question?

Let’s talk

How to Use Leverage Inside a Solo 401(k) or Self-Directed IRA

If you’ve ever looked into investing in real estate using a Self-Directed IRA or Solo 401(k), you’ve probably asked yourself a simple question: Can I use financing, or do I have to pay all cash?

The answer is yes, you can use financing, but it must be done in a very specific way. That structure is called a non-recourse loan, and understanding how it works is essential before moving forward with a deal.

Non-recourse lending is one of the most powerful tools available inside self-directed retirement accounts. It allows you to increase your purchasing power, scale investments faster, and maintain the benefits of tax-advantaged growth. However, it also comes with unique rules, expectations, and tax considerations that investors need to fully understand.

This guide breaks down exactly how non-recourse lending works, when it makes sense, and how to structure it correctly.

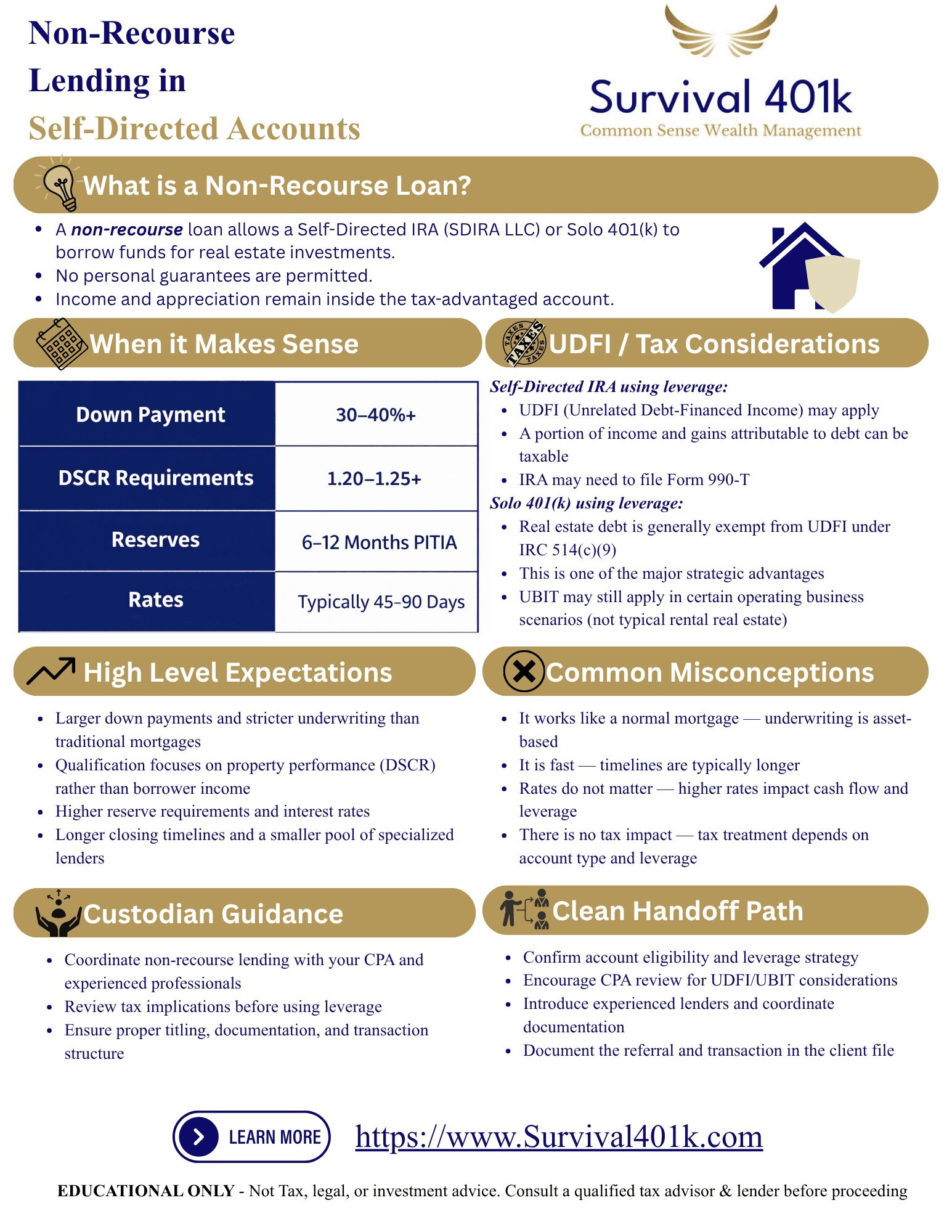

What is a Non-Recourse Loan?

At its core, a non-recourse loan is financing where the retirement account, not you personally, is the borrower.

With a traditional mortgage, you personally guarantee the loan. With a non-recourse loan, the lender’s only security is the property itself. If the loan defaults, the lender cannot pursue your personal assets.

This structure exists because IRS rules prohibit personal guarantees inside retirement accounts. The loan must stand on its own, secured solely by the asset.

Because of this, lenders evaluate deals differently. The focus shifts from borrower income to property performance, which is a key distinction.

When Non-Recourse Lending Makes Sense

This strategy is most effective when you already have capital inside your retirement account but want to scale your investment capacity.

Instead of purchasing one property outright, leverage allows you to control larger assets or multiple properties, increasing both exposure and long-term growth potential.

Lenders primarily evaluate the property’s ability to cover its debt through DSCR (Debt Service Coverage Ratio). In most cases, they want to see a ratio of 1.20–1.25 or higher, meaning the property produces more income than required to service the loan.

You should also expect higher down payments, typically in the 30–40% range, along with reserve requirements to ensure the property can sustain itself.

What to Expect from the Process

While underwriting is primarily asset-based, lenders also assess the retirement account’s liquidity position, the borrower’s real estate experience, and, in some cases, overall creditworthiness. The strength of the property and DSCR remain the primary drivers of approval.

Interest rates are typically higher than conventional loans, which directly impacts cash flow and leverage. This must be factored into deal analysis.

Deals that close smoothly typically begin aligning the lender, custodian, and CPA 30–45 days ahead of the target close. Planning is the variable that most often separates a smooth closing from a stalled one.

The lender pool is also smaller, meaning you are working with specialized institutions that understand self-directed accounts.

Understanding the Tax Side: UDFI and UBIT

One of the most critical aspects of using leverage inside retirement accounts is understanding tax implications.

If a Self-Directed IRA uses leverage, Unrelated Debt-Financed Income (UDFI) may apply. This means a portion of income and gains attributable to the financed portion of the property can be taxable, and the IRA may be required to file Form 990-T.

However, Solo 401(k)s offer a significant structural advantage.

Under IRC 514(c)(9), qualified plans such as Solo 401(k)s are generally exempt from UDFI on leveraged real estate — one of the key structural advantages over a Self-Directed IRA.

This allows rental income and gains to remain fully within the tax-advantaged structure in most real estate scenarios.

That said, UBIT may still apply in certain operating business situations, though this is not typical for passive rental real estate.

“Leverage doesn’t create risk, structure does. When structured correctly, it creates opportunity.”

Garrett Clark

Director of Sales

Prohibited Transactions (Critical to Understand)

Any discussion of real estate inside a retirement account must include prohibited transaction rules under IRC 4975.

These rules prohibit self-dealing and transactions with disqualified persons, which include yourself, your spouse, your parents or children, and certain business entities you control.

You cannot live in the property, personally benefit from it, perform unpaid work that materially benefits the investment, or mix personal and retirement funds.

Violating these rules can disqualify the entire retirement account, making this one of the most important areas to get right.

Example Deal Structure

To make this more concrete, here’s a simplified example:

An investor has $200,000 in a Solo 401(k). They use that as a 35% down payment to acquire a $570,000 rental property using non-recourse financing.

The property meets a DSCR of 1.25 and generates positive cash flow.

All rental income flows back into the Solo 401(k), and all expenses are paid from the account. Over time, both cash flow and appreciation accumulate within the tax-advantaged structure.

This is how leverage allows investors to scale beyond what cash-only purchases would allow.

When NOT to Use Non-Recourse Lending

While powerful, this strategy is not always appropriate.

It may not make sense in low cash flow deals with thin margins, high-interest-rate environments where leverage reduces profitability, short-term flips where timelines and costs don’t align, or deals where liquidity is insufficient to cover reserves and expenses.

Understanding when not to use leverage builds long-term success and avoids unnecessary risk.

The Importance of Proper Guidance

Because of the complexity involved, non-recourse lending should always be approached with a team.

This includes your CPA, lender, and plan provider working together to ensure proper structuring, accurate tax treatment, and compliance with IRS rules.

Proper titling, documentation, and transaction flow are critical to maintaining the integrity of the retirement account.

The Bottom Line

Non-recourse lending allows you to scale real estate investments inside a retirement account without personal liability while maintaining tax advantages.

The key differentiator is structure.

Solo 401(k)s, in particular, provide a significant advantage due to their exemption from UDFI on real estate debt, making them one of the most efficient vehicles for leveraged real estate investing.

When executed correctly, this strategy can transform a retirement account into a long-term wealth-building engine.

Next Step

If you’re evaluating whether your deal is structured correctly for a Solo 401(k) or non-recourse financing, the best first step is a quick strategy call before moving forward.

You can schedule a time directly here:

https://www.survival401k.com

Or reach out to us directly:

info@survival401k.com

210-264-2075

A properly structured deal at the beginning can save significant time, taxes, and risk later.

This content is for educational purposes only and is not tax, legal, or investment advice. Please consult a qualified professional before making any financial or investment decisions.

Prohibited Transactions (Critical to Understand)

Any discussion of real estate inside a retirement account must include prohibited transaction rules under IRC 4975.

These rules prohibit self-dealing and transactions with disqualified persons, which include yourself, your spouse, your parents or children, and certain business entities you control.

You cannot live in the property, personally benefit from it, perform unpaid work that materially benefits the investment, or mix personal and retirement funds.

Violating these rules can disqualify the entire retirement account, making this one of the most important areas to get right.

Example Deal Structure

To make this more concrete, here’s a simplified example:

An investor has $200,000 in a Solo 401(k). They use that as a 35% down payment to acquire a $570,000 rental property using non-recourse financing.

The property meets a DSCR of 1.25 and generates positive cash flow.

All rental income flows back into the Solo 401(k), and all expenses are paid from the account. Over time, both cash flow and appreciation accumulate within the tax-advantaged structure.

This is how leverage allows investors to scale beyond what cash-only purchases would allow.

When NOT to Use Non-Recourse Lending

While powerful, this strategy is not always appropriate.

It may not make sense in low cash flow deals with thin margins, high-interest-rate environments where leverage reduces profitability, short-term flips where timelines and costs don’t align, or deals where liquidity is insufficient to cover reserves and expenses.

Understanding when not to use leverage builds long-term success and avoids unnecessary risk.

The Importance of Proper Guidance

Because of the complexity involved, non-recourse lending should always be approached with a team.

This includes your CPA, lender, and plan provider working together to ensure proper structuring, accurate tax treatment, and compliance with IRS rules.

Proper titling, documentation, and transaction flow are critical to maintaining the integrity of the retirement account.

The Bottom Line

Non-recourse lending allows you to scale real estate investments inside a retirement account without personal liability while maintaining tax advantages.

The key differentiator is structure.

Solo 401(k)s, in particular, provide a significant advantage due to their exemption from UDFI on real estate debt, making them one of the most efficient vehicles for leveraged real estate investing.

When executed correctly, this strategy can transform a retirement account into a long-term wealth-building engine.

Next Step

If you’re evaluating whether your deal is structured correctly for a Solo 401(k) or non-recourse financing, the best first step is a quick strategy call before moving forward.

You can schedule a time directly here:

https://www.survival401k.com

Or reach out to us directly:

info@survival401k.com

210-264-2075

A properly structured deal at the beginning can save significant time, taxes, and risk later.

This content is for educational purposes only and is not tax, legal, or investment advice. Please consult a qualified professional before making any financial or investment decisions.

How to Use Leverage Inside a Solo 401(k) or Self-Directed IRA

If you’ve ever looked into investing in real estate using a Self-Directed IRA or Solo 401(k), you’ve probably asked yourself a simple question: Can I use financing, or do I have to pay all cash?

The answer is yes, you can use financing, but it must be done in a very specific way. That structure is called a non-recourse loan, and understanding how it works is essential before moving forward with a deal.

Non-recourse lending is one of the most powerful tools available inside self-directed retirement accounts. It allows you to increase your purchasing power, scale investments faster, and maintain the benefits of tax-advantaged growth. However, it also comes with unique rules, expectations, and tax considerations that investors need to fully understand.

This guide breaks down exactly how non-recourse lending works, when it makes sense, and how to structure it correctly.

What is a Non-Recourse Loan?

At its core, a non-recourse loan is financing where the retirement account, not you personally, is the borrower.

With a traditional mortgage, you personally guarantee the loan. With a non-recourse loan, the lender’s only security is the property itself. If the loan defaults, the lender cannot pursue your personal assets.

This structure exists because IRS rules prohibit personal guarantees inside retirement accounts. The loan must stand on its own, secured solely by the asset.

Because of this, lenders evaluate deals differently. The focus shifts from borrower income to property performance, which is a key distinction.

When Non-Recourse Lending Makes Sense

This strategy is most effective when you already have capital inside your retirement account but want to scale your investment capacity.

Instead of purchasing one property outright, leverage allows you to control larger assets or multiple properties, increasing both exposure and long-term growth potential.

Lenders primarily evaluate the property’s ability to cover its debt through DSCR (Debt Service Coverage Ratio). In most cases, they want to see a ratio of 1.20–1.25 or higher, meaning the property produces more income than required to service the loan.

You should also expect higher down payments, typically in the 30–40% range, along with reserve requirements to ensure the property can sustain itself.

What to Expect from the Process

While underwriting is primarily asset-based, lenders also assess the retirement account’s liquidity position, the borrower’s real estate experience, and, in some cases, overall creditworthiness. The strength of the property and DSCR remain the primary drivers of approval.

Interest rates are typically higher than conventional loans, which directly impacts cash flow and leverage. This must be factored into deal analysis.

Deals that close smoothly typically begin aligning the lender, custodian, and CPA 30–45 days ahead of the target close. Planning is the variable that most often separates a smooth closing from a stalled one.

The lender pool is also smaller, meaning you are working with specialized institutions that understand self-directed accounts.

Understanding the Tax Side: UDFI and UBIT

One of the most critical aspects of using leverage inside retirement accounts is understanding tax implications.

If a Self-Directed IRA uses leverage, Unrelated Debt-Financed Income (UDFI) may apply. This means a portion of income and gains attributable to the financed portion of the property can be taxable, and the IRA may be required to file Form 990-T.

However, Solo 401(k)s offer a significant structural advantage.

Under IRC 514(c)(9), qualified plans such as Solo 401(k)s are generally exempt from UDFI on leveraged real estate — one of the key structural advantages over a Self-Directed IRA.

This allows rental income and gains to remain fully within the tax-advantaged structure in most real estate scenarios.

That said, UBIT may still apply in certain operating business situations, though this is not typical for passive rental real estate.

“Leverage doesn’t create risk, structure does. When structured correctly, it creates opportunity.”

Garrett Clark

Director of Sales

Prohibited Transactions (Critical to Understand)

Any discussion of real estate inside a retirement account must include prohibited transaction rules under IRC 4975.

These rules prohibit self-dealing and transactions with disqualified persons, which include yourself, your spouse, your parents or children, and certain business entities you control.

You cannot live in the property, personally benefit from it, perform unpaid work that materially benefits the investment, or mix personal and retirement funds.

Violating these rules can disqualify the entire retirement account, making this one of the most important areas to get right.

Example Deal Structure

To make this more concrete, here’s a simplified example:

An investor has $200,000 in a Solo 401(k). They use that as a 35% down payment to acquire a $570,000 rental property using non-recourse financing.

The property meets a DSCR of 1.25 and generates positive cash flow.

All rental income flows back into the Solo 401(k), and all expenses are paid from the account. Over time, both cash flow and appreciation accumulate within the tax-advantaged structure.

This is how leverage allows investors to scale beyond what cash-only purchases would allow.

When NOT to Use Non-Recourse Lending

While powerful, this strategy is not always appropriate.

It may not make sense in low cash flow deals with thin margins, high-interest-rate environments where leverage reduces profitability, short-term flips where timelines and costs don’t align, or deals where liquidity is insufficient to cover reserves and expenses.

Understanding when not to use leverage builds long-term success and avoids unnecessary risk.

The Importance of Proper Guidance

Because of the complexity involved, non-recourse lending should always be approached with a team.

This includes your CPA, lender, and plan provider working together to ensure proper structuring, accurate tax treatment, and compliance with IRS rules.

Proper titling, documentation, and transaction flow are critical to maintaining the integrity of the retirement account.

The Bottom Line

Non-recourse lending allows you to scale real estate investments inside a retirement account without personal liability while maintaining tax advantages.

The key differentiator is structure.

Solo 401(k)s, in particular, provide a significant advantage due to their exemption from UDFI on real estate debt, making them one of the most efficient vehicles for leveraged real estate investing.

When executed correctly, this strategy can transform a retirement account into a long-term wealth-building engine.

Next Step

If you’re evaluating whether your deal is structured correctly for a Solo 401(k) or non-recourse financing, the best first step is a quick strategy call before moving forward.

You can schedule a time directly here:

https://www.survival401k.com

Or reach out to us directly:

info@survival401k.com

210-264-2075

A properly structured deal at the beginning can save significant time, taxes, and risk later.

This content is for educational purposes only and is not tax, legal, or investment advice. Please consult a qualified professional before making any financial or investment decisions.