by

Garrett Clark

Investment Guidance

Private Lending Through a Solo 401(k)

Discover how private lending through a self-directed Solo 401(k) can open the door to alternative investment opportunities beyond stocks and mutual funds. In this guide, we explore how private lending works, potential benefits and risks, IRS rules to understand, and best practices for structuring loans within your retirement plan. Whether you're interested in lending to real estate investors, entrepreneurs, or small businesses, learn how a Solo 401(k) can provide the flexibility to potentially generate income while maintaining the tax advantages of a qualified retirement account.

Search

Search

Category

Any Question?

Let’s talk

Any Question?

Let’s talk

Search

Search

Category

Any Question?

Let’s talk

For many investors, retirement accounts are synonymous with stocks, mutual funds, ETFs, and bonds. While these traditional investments have helped millions build wealth, they are not the only options available. One of the most overlooked opportunities within a self-directed Solo 401(k) is private lending.

Private lending allows retirement investors to act as the lender instead of the borrower. Rather than investing in public markets, your Solo 401(k) can potentially generate returns by making loans to individuals, businesses, or real estate investors. When structured properly and in accordance with IRS rules, private lending can offer diversification, predictable income, and greater control over how retirement capital is deployed.

In this guide, we'll explore how private lending works inside a Solo 401(k), potential benefits and risks, IRS considerations, and best practices for getting started.

What Is Private Lending?

Private lending is the practice of providing capital directly to a borrower in exchange for agreed-upon repayment terms and interest.

Instead of depositing money into a savings account or purchasing publicly traded investments, a lender uses their funds to finance a loan. The borrower agrees to repay the principal plus interest according to the terms outlined in a promissory note or loan agreement.

Private lending opportunities can include:

Real estate investors seeking funding for purchases or renovations

House flippers needing short-term capital

Small business owners requiring financing

Entrepreneurs launching new ventures

Bridge loans for investment projects

Asset-backed loans secured by collateral

Within a self-directed Solo 401(k), the retirement plan—not the account owner personally—becomes the lender.

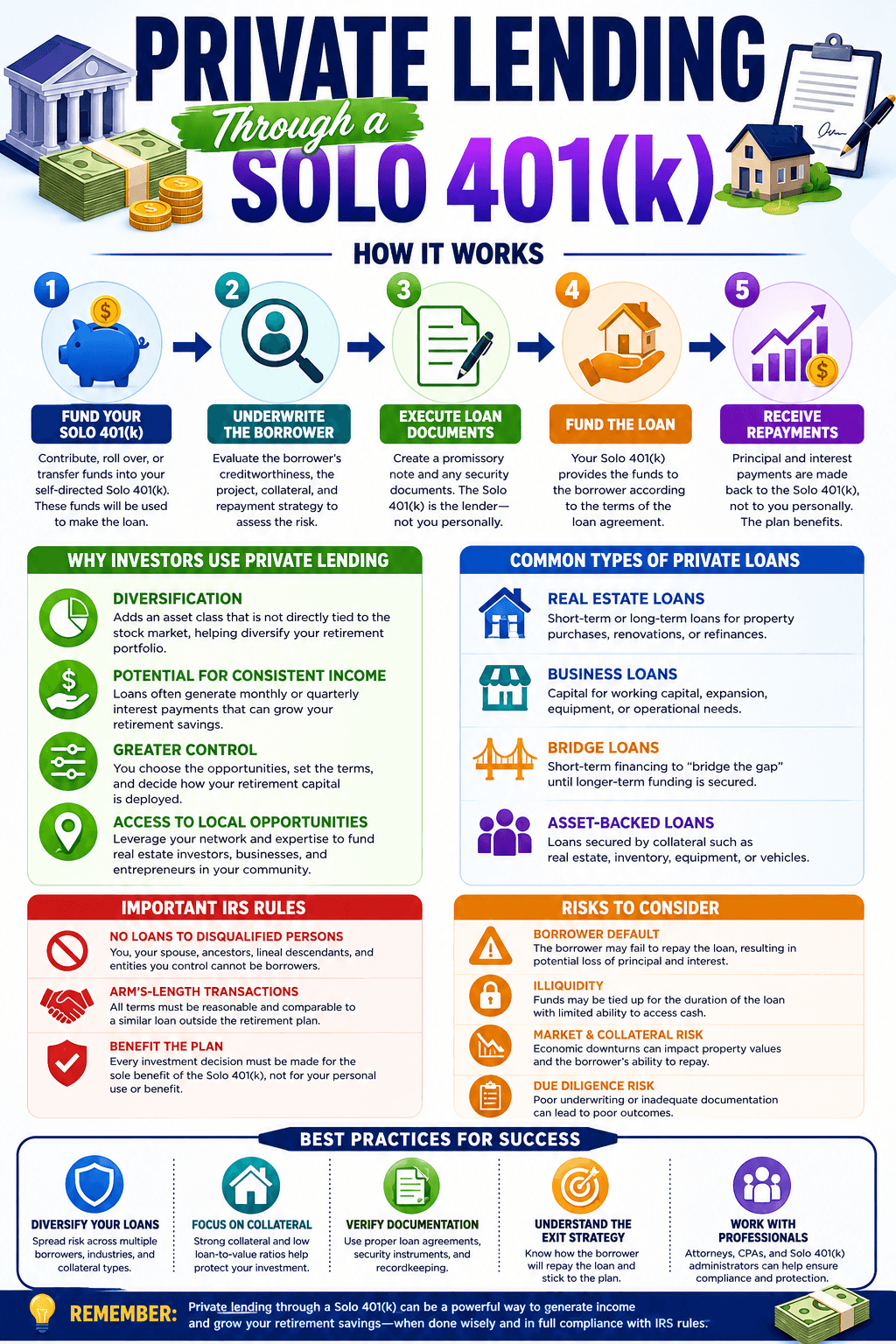

Why Investors Use Private Lending in a Solo 401(k)

Many self-directed investors are attracted to private lending because it provides an alternative source of returns that may not be directly tied to stock market performance.

Benefits can include:

Diversification

Traditional retirement accounts often have significant exposure to the stock and bond markets. Private lending allows investors to add another asset class that may perform differently from public markets.

Rather than relying solely on market appreciation, lenders earn returns through contractual interest payments.

Potential for Consistent Cash Flow

Many private loans include monthly, quarterly, or lump-sum interest payments.

This creates the possibility of generating recurring income back into the Solo 401(k), which can then be reinvested into future opportunities.

Greater Control

Unlike mutual funds where investors have little say over underlying investments, private lending allows investors to evaluate borrowers, structure terms, determine collateral requirements, and select projects they believe fit their risk tolerance.

Access to Local Opportunities

Many investors discover lending opportunities through professional networks, local real estate communities, business relationships, or industry connections.

A Solo 401(k) provides the flexibility to pursue opportunities that may not be available through traditional brokerage accounts.

How Private Lending Works Inside a Solo 401(k)

The process is relatively straightforward.

Step 1: Establish a Self-Directed Solo 401(k)

A self-directed Solo 401(k) provides the investment flexibility necessary to make private loans.

Unlike many traditional retirement accounts that limit investment options, a properly structured Solo 401(k) allows alternative investments, including private lending.

Step 2: Fund the Plan

Funds can come from:

Annual contributions

Rollovers from former employer plans

Transfers from eligible retirement accounts

Existing Solo 401(k) assets

Once funds are available, the plan can begin evaluating lending opportunities.

Step 3: Underwrite the Borrower

Before issuing a loan, investors should conduct due diligence.

Areas to evaluate include:

Borrower creditworthiness

Project viability

Exit strategy

Available collateral

Loan-to-value ratios

Experience of the borrower

Market conditions

The goal is to assess both repayment ability and overall risk.

Step 4: Execute Loan Documents

The loan should be properly documented through:

Promissory notes

Security agreements

Deeds of trust or mortgages (if applicable)

Personal guarantees (if applicable)

Collateral documentation

All documents should clearly identify the Solo 401(k) as the lender.

Step 5: Receive Repayments

Principal and interest payments must flow directly back into the Solo 401(k).

The account owner should never receive payments personally.

All income generated belongs to the retirement plan.

Real Estate Lending: A Popular Strategy

One of the most common uses of private lending within a Solo 401(k) involves real estate investing.

For example:

A real estate investor finds a property needing renovation.

They require short-term financing to purchase and improve the property before selling it.

Your Solo 401(k) may provide a loan secured by the property.

The borrower agrees to:

Pay interest

Repay principal

Follow agreed loan terms

If the project succeeds, the Solo 401(k) receives the agreed-upon return.

Because many real estate loans are secured by physical property, some investors view this as an additional layer of protection compared to unsecured lending.

Understanding Secured vs. Unsecured Loans

Secured Loans

Secured loans are backed by collateral.

Examples include:

Real estate

Equipment

Vehicles

Business assets

If the borrower defaults, the lender may have legal rights to pursue the collateral.

Unsecured Loans

Unsecured loans rely primarily on the borrower's creditworthiness and promise to repay.

These loans often carry higher risk because there is no specific asset securing the obligation.

Many private lenders prefer secured lending whenever possible.

Important IRS Rules to Understand

Although Solo 401(k)s provide substantial investment flexibility, investors must still follow IRS regulations.

Prohibited Transactions

A Solo 401(k) cannot make loans to disqualified persons.

Disqualified persons generally include:

The account owner

Spouse

Parents

Grandparents

Children

Grandchildren

Certain entities owned by these individuals

For example:

Your Solo 401(k) cannot lend money to:

Yourself

Your spouse

Your child

A company you personally own

Violating prohibited transaction rules can result in severe tax consequences.

Arm's-Length Transactions

All loans should be conducted as legitimate business transactions.

Terms should be reasonable and properly documented.

The Solo 401(k) must be treated as a separate legal entity.

Benefit to the Plan

Every investment decision must primarily benefit the retirement plan—not the account holder personally.

Risks of Private Lending

Like any investment strategy, private lending involves risk.

Borrower Default

The biggest risk is that a borrower fails to repay the loan.

This can lead to:

Delayed payments

Foreclosure proceedings

Legal expenses

Potential loss of capital

Liquidity Risk

Unlike publicly traded investments, private loans are not easily sold.

Capital may remain tied up until the loan matures.

Market Risk

Changes in economic conditions can impact borrowers and collateral values.

For example, a downturn in real estate markets may affect property-backed loans.

Due Diligence Risk

Poor underwriting can lead to bad lending decisions.

Investors should carefully evaluate every opportunity before committing retirement funds.

Best Practices for Solo 401(k) Private Lending

Diversify Loans

Avoid placing all retirement capital into a single borrower or project.

Diversification may help reduce overall risk.

Focus on Collateral

Whenever possible, seek strong collateral that supports the loan.

Many lenders prioritize low loan-to-value ratios.

Verify Documentation

Ensure all agreements are professionally prepared and properly executed.

Clear documentation helps protect the lender's interests.

Understand the Exit Strategy

Always ask:

"How will the borrower repay this loan?"

A strong exit strategy is often one of the most important indicators of a quality lending opportunity.

Work With Professionals

Consider consulting:

Attorneys

Title companies

Escrow companies

Tax professionals

Solo 401(k) specialists

Experienced professionals can help ensure transactions are structured properly.

Who Should Consider Private Lending?

Private lending may appeal to investors who:

Want alternatives to traditional investments

Prefer generating interest income

Have experience evaluating deals

Understand risk management

Desire greater control over retirement assets

Want exposure to real estate-related opportunities without directly owning property

It may be especially attractive for entrepreneurs, real estate professionals, and investors who already have lending opportunities available through their networks.

Final Thoughts

Private lending through a Solo 401(k) offers a unique way to put retirement capital to work outside of traditional Wall Street investments. By acting as the lender, investors may potentially generate interest income, diversify retirement holdings, and gain greater control over how their retirement funds are invested.

However, success requires careful due diligence, proper documentation, sound underwriting practices, and strict compliance with IRS regulations. Investors should thoroughly evaluate each opportunity and understand both the potential rewards and risks before committing retirement assets.

For those looking to expand beyond stocks and mutual funds, private lending may be one of the most powerful alternative investment strategies available within a self-directed Solo 401(k). When used responsibly, it can become a valuable component of a diversified retirement portfolio and a meaningful tool for long-term wealth building.

This blog is not tax or financial advice and is for educational purposes only. Please consult a professional before making any investment choices since everyone's situation is different.

For many investors, retirement accounts are synonymous with stocks, mutual funds, ETFs, and bonds. While these traditional investments have helped millions build wealth, they are not the only options available. One of the most overlooked opportunities within a self-directed Solo 401(k) is private lending.

Private lending allows retirement investors to act as the lender instead of the borrower. Rather than investing in public markets, your Solo 401(k) can potentially generate returns by making loans to individuals, businesses, or real estate investors. When structured properly and in accordance with IRS rules, private lending can offer diversification, predictable income, and greater control over how retirement capital is deployed.

In this guide, we'll explore how private lending works inside a Solo 401(k), potential benefits and risks, IRS considerations, and best practices for getting started.

What Is Private Lending?

Private lending is the practice of providing capital directly to a borrower in exchange for agreed-upon repayment terms and interest.

Instead of depositing money into a savings account or purchasing publicly traded investments, a lender uses their funds to finance a loan. The borrower agrees to repay the principal plus interest according to the terms outlined in a promissory note or loan agreement.

Private lending opportunities can include:

Real estate investors seeking funding for purchases or renovations

House flippers needing short-term capital

Small business owners requiring financing

Entrepreneurs launching new ventures

Bridge loans for investment projects

Asset-backed loans secured by collateral

Within a self-directed Solo 401(k), the retirement plan—not the account owner personally—becomes the lender.

Why Investors Use Private Lending in a Solo 401(k)

Many self-directed investors are attracted to private lending because it provides an alternative source of returns that may not be directly tied to stock market performance.

Benefits can include:

Diversification

Traditional retirement accounts often have significant exposure to the stock and bond markets. Private lending allows investors to add another asset class that may perform differently from public markets.

Rather than relying solely on market appreciation, lenders earn returns through contractual interest payments.

Potential for Consistent Cash Flow

Many private loans include monthly, quarterly, or lump-sum interest payments.

This creates the possibility of generating recurring income back into the Solo 401(k), which can then be reinvested into future opportunities.

Greater Control

Unlike mutual funds where investors have little say over underlying investments, private lending allows investors to evaluate borrowers, structure terms, determine collateral requirements, and select projects they believe fit their risk tolerance.

Access to Local Opportunities

Many investors discover lending opportunities through professional networks, local real estate communities, business relationships, or industry connections.

A Solo 401(k) provides the flexibility to pursue opportunities that may not be available through traditional brokerage accounts.

How Private Lending Works Inside a Solo 401(k)

The process is relatively straightforward.

Step 1: Establish a Self-Directed Solo 401(k)

A self-directed Solo 401(k) provides the investment flexibility necessary to make private loans.

Unlike many traditional retirement accounts that limit investment options, a properly structured Solo 401(k) allows alternative investments, including private lending.

Step 2: Fund the Plan

Funds can come from:

Annual contributions

Rollovers from former employer plans

Transfers from eligible retirement accounts

Existing Solo 401(k) assets

Once funds are available, the plan can begin evaluating lending opportunities.

Step 3: Underwrite the Borrower

Before issuing a loan, investors should conduct due diligence.

Areas to evaluate include:

Borrower creditworthiness

Project viability

Exit strategy

Available collateral

Loan-to-value ratios

Experience of the borrower

Market conditions

The goal is to assess both repayment ability and overall risk.

Step 4: Execute Loan Documents

The loan should be properly documented through:

Promissory notes

Security agreements

Deeds of trust or mortgages (if applicable)

Personal guarantees (if applicable)

Collateral documentation

All documents should clearly identify the Solo 401(k) as the lender.

Step 5: Receive Repayments

Principal and interest payments must flow directly back into the Solo 401(k).

The account owner should never receive payments personally.

All income generated belongs to the retirement plan.

Real Estate Lending: A Popular Strategy

One of the most common uses of private lending within a Solo 401(k) involves real estate investing.

For example:

A real estate investor finds a property needing renovation.

They require short-term financing to purchase and improve the property before selling it.

Your Solo 401(k) may provide a loan secured by the property.

The borrower agrees to:

Pay interest

Repay principal

Follow agreed loan terms

If the project succeeds, the Solo 401(k) receives the agreed-upon return.

Because many real estate loans are secured by physical property, some investors view this as an additional layer of protection compared to unsecured lending.

Understanding Secured vs. Unsecured Loans

Secured Loans

Secured loans are backed by collateral.

Examples include:

Real estate

Equipment

Vehicles

Business assets

If the borrower defaults, the lender may have legal rights to pursue the collateral.

Unsecured Loans

Unsecured loans rely primarily on the borrower's creditworthiness and promise to repay.

These loans often carry higher risk because there is no specific asset securing the obligation.

Many private lenders prefer secured lending whenever possible.

Important IRS Rules to Understand

Although Solo 401(k)s provide substantial investment flexibility, investors must still follow IRS regulations.

Prohibited Transactions

A Solo 401(k) cannot make loans to disqualified persons.

Disqualified persons generally include:

The account owner

Spouse

Parents

Grandparents

Children

Grandchildren

Certain entities owned by these individuals

For example:

Your Solo 401(k) cannot lend money to:

Yourself

Your spouse

Your child

A company you personally own

Violating prohibited transaction rules can result in severe tax consequences.

Arm's-Length Transactions

All loans should be conducted as legitimate business transactions.

Terms should be reasonable and properly documented.

The Solo 401(k) must be treated as a separate legal entity.

Benefit to the Plan

Every investment decision must primarily benefit the retirement plan—not the account holder personally.

Risks of Private Lending

Like any investment strategy, private lending involves risk.

Borrower Default

The biggest risk is that a borrower fails to repay the loan.

This can lead to:

Delayed payments

Foreclosure proceedings

Legal expenses

Potential loss of capital

Liquidity Risk

Unlike publicly traded investments, private loans are not easily sold.

Capital may remain tied up until the loan matures.

Market Risk

Changes in economic conditions can impact borrowers and collateral values.

For example, a downturn in real estate markets may affect property-backed loans.

Due Diligence Risk

Poor underwriting can lead to bad lending decisions.

Investors should carefully evaluate every opportunity before committing retirement funds.

Best Practices for Solo 401(k) Private Lending

Diversify Loans

Avoid placing all retirement capital into a single borrower or project.

Diversification may help reduce overall risk.

Focus on Collateral

Whenever possible, seek strong collateral that supports the loan.

Many lenders prioritize low loan-to-value ratios.

Verify Documentation

Ensure all agreements are professionally prepared and properly executed.

Clear documentation helps protect the lender's interests.

Understand the Exit Strategy

Always ask:

"How will the borrower repay this loan?"

A strong exit strategy is often one of the most important indicators of a quality lending opportunity.

Work With Professionals

Consider consulting:

Attorneys

Title companies

Escrow companies

Tax professionals

Solo 401(k) specialists

Experienced professionals can help ensure transactions are structured properly.

Who Should Consider Private Lending?

Private lending may appeal to investors who:

Want alternatives to traditional investments

Prefer generating interest income

Have experience evaluating deals

Understand risk management

Desire greater control over retirement assets

Want exposure to real estate-related opportunities without directly owning property

It may be especially attractive for entrepreneurs, real estate professionals, and investors who already have lending opportunities available through their networks.

Final Thoughts

Private lending through a Solo 401(k) offers a unique way to put retirement capital to work outside of traditional Wall Street investments. By acting as the lender, investors may potentially generate interest income, diversify retirement holdings, and gain greater control over how their retirement funds are invested.

However, success requires careful due diligence, proper documentation, sound underwriting practices, and strict compliance with IRS regulations. Investors should thoroughly evaluate each opportunity and understand both the potential rewards and risks before committing retirement assets.

For those looking to expand beyond stocks and mutual funds, private lending may be one of the most powerful alternative investment strategies available within a self-directed Solo 401(k). When used responsibly, it can become a valuable component of a diversified retirement portfolio and a meaningful tool for long-term wealth building.

This blog is not tax or financial advice and is for educational purposes only. Please consult a professional before making any investment choices since everyone's situation is different.