by

Garrett Clark

Estate Planning

Solo 401(k) vs. Trust: Understanding Estate Planning Tools and Their Roles

Many business owners spend years building wealth but overlook one important question: What happens to those assets when you're gone? Estate planning is not just about transferring wealth. It is about protecting your family, reducing complications, maintaining privacy, and ensuring your wishes are carried out efficiently. Two powerful tools that often come up in estate planning discussions are the Solo 401(k) and trusts. While both can play important roles in a comprehensive estate plan, they serve different purposes and offer unique advantages. Understanding how they work together can help business owners and investors create a more complete strategy for preserving and transferring wealth.

Search

Search

Category

Any Question?

Let’s talk

Any Question?

Let’s talk

Search

Search

Category

Any Question?

Let’s talk

Many people assume that once they have accumulated retirement savings, real estate, and investment accounts, their estate plan is complete. However, building wealth and successfully transferring wealth are two entirely different challenges.

Without proper planning, loved ones may face delays, court proceedings, unnecessary expenses, confusion, and potential disputes. Fortunately, several estate planning tools can help reduce these risks.

Two of the most commonly discussed tools are the Solo 401(k) and trusts. While they are often mentioned together, they serve fundamentally different purposes.

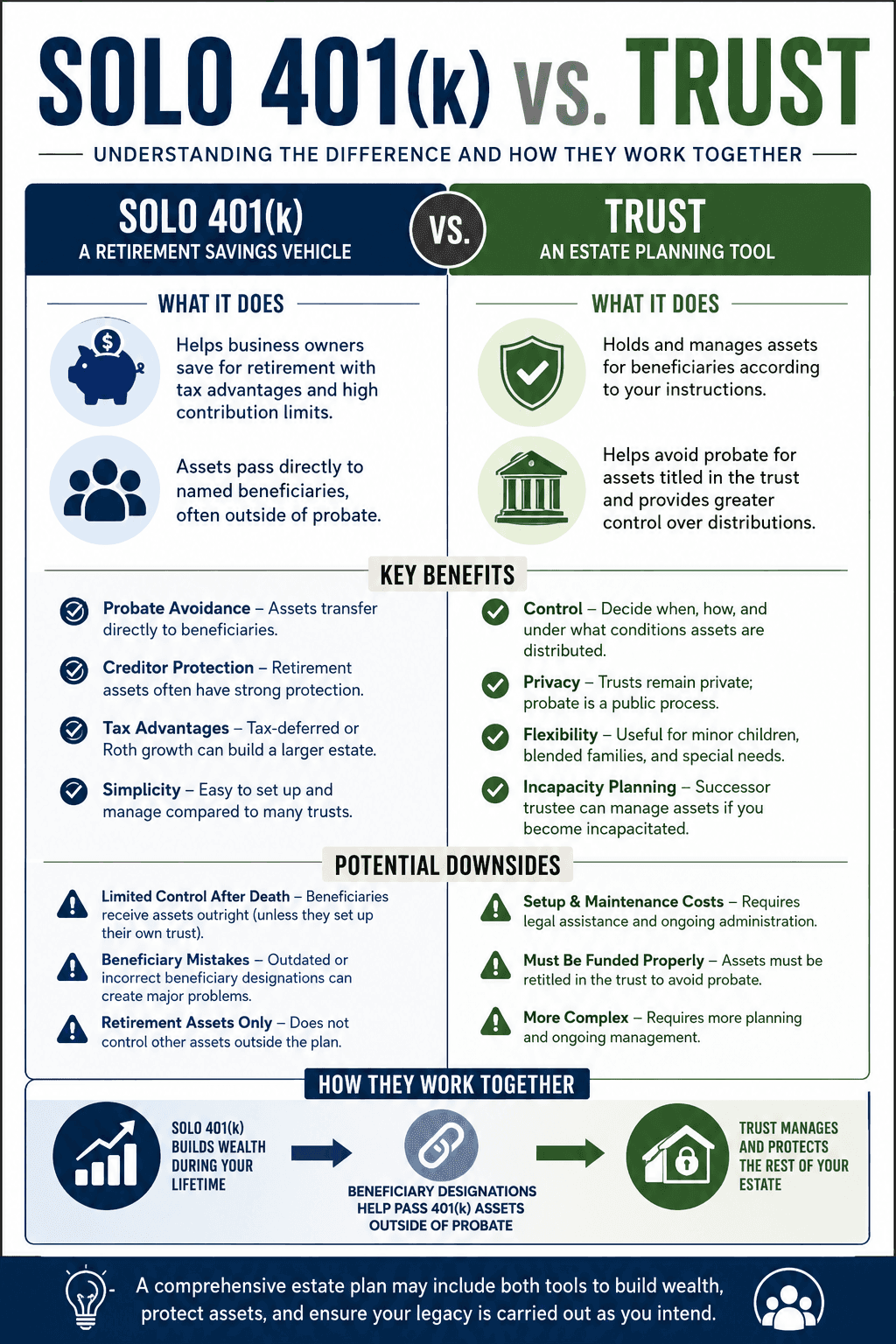

A Solo 401(k) is primarily a retirement savings vehicle that can also provide significant estate planning benefits. A trust, on the other hand, is specifically designed as an estate planning and asset management tool.

Understanding the strengths and limitations of each can help investors build a more complete estate plan.

Understanding Probate

Before comparing trusts and Solo 401(k)s, it is important to understand probate.

Probate is the court-supervised process of administering a deceased person's estate.

During probate, the court typically:

Verifies the validity of a will

Identifies assets

Pays outstanding debts

Resolves disputes

Distributes property to heirs

Probate can be:

Time-consuming

Expensive

Public

Stressful for family members

Depending on the state and complexity of the estate, probate can last months or even years.

Many estate planning strategies focus on reducing or avoiding probate whenever legally possible.

How a Solo 401(k) Fits Into Estate Planning

A Solo 401(k) is primarily designed to help self-employed individuals and business owners save for retirement.

However, many people are surprised to learn that retirement accounts often receive favorable treatment during estate administration.

One major benefit is that properly designated retirement account beneficiaries generally allow assets to pass directly to heirs outside of probate.

This means the assets can often transfer directly to named beneficiaries without becoming part of the probate estate.

For example:

John owns a Solo 401(k) worth $750,000.

His daughter is listed as the primary beneficiary.

When John passes away, the account typically transfers directly to his daughter according to the beneficiary designation rather than passing through probate court.

This can provide significant advantages for heirs.

Benefits of a Solo 401(k) for Estate Planning

Probate Avoidance Through Beneficiary Designations

One of the largest estate planning advantages of a Solo 401(k) is the ability to transfer assets directly to beneficiaries.

This often allows:

Faster asset transfer

Reduced court involvement

Lower administrative costs

Greater privacy

Beneficiary designations generally control the distribution of retirement assets regardless of what a will may state.

Asset Protection During Life

Many retirement accounts receive strong creditor protection under federal and state laws.

While rules vary by jurisdiction, retirement assets often enjoy greater protection than assets held personally.

This protection can be valuable for:

Business owners

Real estate investors

Medical professionals

Individuals in high-liability professions

Tax-Advantaged Growth

Unlike trusts, a Solo 401(k) is fundamentally designed to help accumulate retirement wealth.

Benefits may include:

Tax-deferred growth

Roth growth potential

Potential tax deductions

High contribution limits

These features can help investors build larger estates over time.

Simplicity

Compared to many estate planning structures, a Solo 401(k) can be relatively straightforward to establish and maintain.

Once beneficiaries are properly designated, asset transfers may be significantly simpler than assets requiring probate proceedings.

Limitations of a Solo 401(k) for Estate Planning

While a Solo 401(k) offers valuable benefits, it is not a complete estate planning solution.

Limited Control After Death

Once assets pass to beneficiaries, the original account owner generally loses control over how those assets are managed.

A beneficiary may:

Withdraw funds

Spend assets quickly

Make poor financial decisions

The original owner typically cannot dictate long-term management through the retirement account itself.

Beneficiary Mistakes Can Create Problems

Many estate planning failures occur because beneficiary forms were never updated.

Common issues include:

Ex-spouses remaining beneficiaries

Missing contingent beneficiaries

Outdated family information

Conflicts between estate documents and beneficiary designations

Regular reviews are essential.

Retirement Assets Only

A Solo 401(k) only controls assets held within the plan.

It does not address:

Personal real estate

Bank accounts

Vehicles

Businesses

Personal property

Additional planning tools are often necessary.

Understanding Trusts

A trust is a legal arrangement in which one party holds and manages assets for the benefit of another party.

Trusts can be used for:

Probate avoidance

Wealth transfer

Asset management

Privacy

Incapacity planning

Tax planning

Asset protection

Unlike retirement accounts, trusts are specifically designed to address estate planning concerns.

Benefits of Trusts

Probate Avoidance

One of the most common reasons individuals establish a trust is to avoid probate.

Assets properly titled in the trust often pass according to trust instructions without court involvement.

This can result in:

Faster distributions

Reduced costs

Less family stress

Greater privacy

Control Beyond Death

One of the biggest advantages of trusts is control.

A trust can specify:

When beneficiaries receive assets

How assets are invested

Conditions for distributions

Age requirements

Educational incentives

For example, a trust may provide:

One-third of assets at age 25

One-third at age 30

Remaining assets at age 35

This level of control is difficult to achieve with beneficiary designations alone.

Planning for Minor Children

Trusts are often valuable for families with young children.

Rather than leaving assets directly to minors, a trust can provide professional management until children reach appropriate ages.

Incapacity Planning

Many trusts help address situations where an individual becomes incapacitated.

The successor trustee can step in and manage trust assets without requiring court-appointed guardianship proceedings.

Privacy

Unlike probate proceedings, trusts generally remain private.

This means details regarding:

Assets

Beneficiaries

Distributions

may remain confidential.

Potential Drawbacks of Trusts

Setup Costs

Trusts typically require legal assistance.

This may involve:

Attorney fees

Document preparation

Ongoing reviews

The upfront cost is often greater than simply naming beneficiaries on retirement accounts.

Maintenance Requirements

A trust only controls assets that are properly transferred into the trust.

Many individuals create trusts but never properly fund them.

An unfunded trust may provide little practical benefit.

Complexity

Trusts can be more complex than beneficiary designations.

They often require:

Ongoing administration

Trustee oversight

Legal guidance

Complexity increases as estate size and goals expand.

Solo 401(k) and Trusts Can Work Together

One common misconception is that investors must choose between a Solo 401(k) and a trust.

In reality, they often complement each other.

Think of the Solo 401(k) as a wealth-building vehicle.

Think of the trust as a wealth-transfer vehicle.

The Solo 401(k) helps accumulate retirement assets during life.

The trust helps coordinate how wealth is managed and distributed after death.

Together, they can create a comprehensive estate planning strategy.

Other Important Estate Planning Components

Estate planning typically involves more than just retirement accounts and trusts.

Additional tools often include:

Will

A will helps direct distribution of assets not otherwise controlled by beneficiary designations or trusts.

Durable Power of Attorney

Allows a trusted individual to handle financial matters if incapacity occurs.

Medical Power of Attorney

Authorizes someone to make healthcare decisions when necessary.

Living Will

Provides instructions regarding medical treatment preferences.

Beneficiary Reviews

Regularly reviewing beneficiaries on:

Solo 401(k)s

IRAs

Life insurance policies

Annuities

is one of the simplest yet most important estate planning tasks.

LLC Structures

Many business owners and real estate investors utilize LLCs to help separate assets, organize ownership, and simplify management of investments.

Which Is Better?

The answer depends on the objective.

If the goal is retirement accumulation, tax advantages, and potentially passing retirement assets directly to heirs, a Solo 401(k) provides powerful benefits.

If the goal is long-term control, family wealth management, privacy, incapacity planning, and comprehensive estate planning, a trust may be more appropriate.

For many successful business owners, the strongest strategy is not choosing one over the other.

It is using both.

A properly structured Solo 401(k) can help build substantial retirement wealth while beneficiary designations may allow those assets to pass outside probate. At the same time, a trust can provide additional control, flexibility, and coordination for the rest of an individual's estate.

Final Thoughts

Estate planning is ultimately about more than avoiding taxes or court proceedings. It is about creating clarity, protecting loved ones, and ensuring that the wealth you worked hard to build is transferred according to your wishes.

A Solo 401(k) and a trust serve different purposes, but both can play valuable roles in a comprehensive estate plan. The Solo 401(k) provides a powerful platform for accumulating retirement wealth and potentially transferring those assets outside probate through beneficiary designations. A trust offers greater control, privacy, and long-term management capabilities that extend beyond retirement accounts.

For many entrepreneurs, investors, and self-employed professionals, combining these tools may provide the best opportunity to build wealth, protect assets, and create a lasting legacy for future generations.

This is not investment or legal tax advice; it is for educational purposes only. Consult a professional before making any legal or investment decisions.

Many people assume that once they have accumulated retirement savings, real estate, and investment accounts, their estate plan is complete. However, building wealth and successfully transferring wealth are two entirely different challenges.

Without proper planning, loved ones may face delays, court proceedings, unnecessary expenses, confusion, and potential disputes. Fortunately, several estate planning tools can help reduce these risks.

Two of the most commonly discussed tools are the Solo 401(k) and trusts. While they are often mentioned together, they serve fundamentally different purposes.

A Solo 401(k) is primarily a retirement savings vehicle that can also provide significant estate planning benefits. A trust, on the other hand, is specifically designed as an estate planning and asset management tool.

Understanding the strengths and limitations of each can help investors build a more complete estate plan.

Understanding Probate

Before comparing trusts and Solo 401(k)s, it is important to understand probate.

Probate is the court-supervised process of administering a deceased person's estate.

During probate, the court typically:

Verifies the validity of a will

Identifies assets

Pays outstanding debts

Resolves disputes

Distributes property to heirs

Probate can be:

Time-consuming

Expensive

Public

Stressful for family members

Depending on the state and complexity of the estate, probate can last months or even years.

Many estate planning strategies focus on reducing or avoiding probate whenever legally possible.

How a Solo 401(k) Fits Into Estate Planning

A Solo 401(k) is primarily designed to help self-employed individuals and business owners save for retirement.

However, many people are surprised to learn that retirement accounts often receive favorable treatment during estate administration.

One major benefit is that properly designated retirement account beneficiaries generally allow assets to pass directly to heirs outside of probate.

This means the assets can often transfer directly to named beneficiaries without becoming part of the probate estate.

For example:

John owns a Solo 401(k) worth $750,000.

His daughter is listed as the primary beneficiary.

When John passes away, the account typically transfers directly to his daughter according to the beneficiary designation rather than passing through probate court.

This can provide significant advantages for heirs.

Benefits of a Solo 401(k) for Estate Planning

Probate Avoidance Through Beneficiary Designations

One of the largest estate planning advantages of a Solo 401(k) is the ability to transfer assets directly to beneficiaries.

This often allows:

Faster asset transfer

Reduced court involvement

Lower administrative costs

Greater privacy

Beneficiary designations generally control the distribution of retirement assets regardless of what a will may state.

Asset Protection During Life

Many retirement accounts receive strong creditor protection under federal and state laws.

While rules vary by jurisdiction, retirement assets often enjoy greater protection than assets held personally.

This protection can be valuable for:

Business owners

Real estate investors

Medical professionals

Individuals in high-liability professions

Tax-Advantaged Growth

Unlike trusts, a Solo 401(k) is fundamentally designed to help accumulate retirement wealth.

Benefits may include:

Tax-deferred growth

Roth growth potential

Potential tax deductions

High contribution limits

These features can help investors build larger estates over time.

Simplicity

Compared to many estate planning structures, a Solo 401(k) can be relatively straightforward to establish and maintain.

Once beneficiaries are properly designated, asset transfers may be significantly simpler than assets requiring probate proceedings.

Limitations of a Solo 401(k) for Estate Planning

While a Solo 401(k) offers valuable benefits, it is not a complete estate planning solution.

Limited Control After Death

Once assets pass to beneficiaries, the original account owner generally loses control over how those assets are managed.

A beneficiary may:

Withdraw funds

Spend assets quickly

Make poor financial decisions

The original owner typically cannot dictate long-term management through the retirement account itself.

Beneficiary Mistakes Can Create Problems

Many estate planning failures occur because beneficiary forms were never updated.

Common issues include:

Ex-spouses remaining beneficiaries

Missing contingent beneficiaries

Outdated family information

Conflicts between estate documents and beneficiary designations

Regular reviews are essential.

Retirement Assets Only

A Solo 401(k) only controls assets held within the plan.

It does not address:

Personal real estate

Bank accounts

Vehicles

Businesses

Personal property

Additional planning tools are often necessary.

Understanding Trusts

A trust is a legal arrangement in which one party holds and manages assets for the benefit of another party.

Trusts can be used for:

Probate avoidance

Wealth transfer

Asset management

Privacy

Incapacity planning

Tax planning

Asset protection

Unlike retirement accounts, trusts are specifically designed to address estate planning concerns.

Benefits of Trusts

Probate Avoidance

One of the most common reasons individuals establish a trust is to avoid probate.

Assets properly titled in the trust often pass according to trust instructions without court involvement.

This can result in:

Faster distributions

Reduced costs

Less family stress

Greater privacy

Control Beyond Death

One of the biggest advantages of trusts is control.

A trust can specify:

When beneficiaries receive assets

How assets are invested

Conditions for distributions

Age requirements

Educational incentives

For example, a trust may provide:

One-third of assets at age 25

One-third at age 30

Remaining assets at age 35

This level of control is difficult to achieve with beneficiary designations alone.

Planning for Minor Children

Trusts are often valuable for families with young children.

Rather than leaving assets directly to minors, a trust can provide professional management until children reach appropriate ages.

Incapacity Planning

Many trusts help address situations where an individual becomes incapacitated.

The successor trustee can step in and manage trust assets without requiring court-appointed guardianship proceedings.

Privacy

Unlike probate proceedings, trusts generally remain private.

This means details regarding:

Assets

Beneficiaries

Distributions

may remain confidential.

Potential Drawbacks of Trusts

Setup Costs

Trusts typically require legal assistance.

This may involve:

Attorney fees

Document preparation

Ongoing reviews

The upfront cost is often greater than simply naming beneficiaries on retirement accounts.

Maintenance Requirements

A trust only controls assets that are properly transferred into the trust.

Many individuals create trusts but never properly fund them.

An unfunded trust may provide little practical benefit.

Complexity

Trusts can be more complex than beneficiary designations.

They often require:

Ongoing administration

Trustee oversight

Legal guidance

Complexity increases as estate size and goals expand.

Solo 401(k) and Trusts Can Work Together

One common misconception is that investors must choose between a Solo 401(k) and a trust.

In reality, they often complement each other.

Think of the Solo 401(k) as a wealth-building vehicle.

Think of the trust as a wealth-transfer vehicle.

The Solo 401(k) helps accumulate retirement assets during life.

The trust helps coordinate how wealth is managed and distributed after death.

Together, they can create a comprehensive estate planning strategy.

Other Important Estate Planning Components

Estate planning typically involves more than just retirement accounts and trusts.

Additional tools often include:

Will

A will helps direct distribution of assets not otherwise controlled by beneficiary designations or trusts.

Durable Power of Attorney

Allows a trusted individual to handle financial matters if incapacity occurs.

Medical Power of Attorney

Authorizes someone to make healthcare decisions when necessary.

Living Will

Provides instructions regarding medical treatment preferences.

Beneficiary Reviews

Regularly reviewing beneficiaries on:

Solo 401(k)s

IRAs

Life insurance policies

Annuities

is one of the simplest yet most important estate planning tasks.

LLC Structures

Many business owners and real estate investors utilize LLCs to help separate assets, organize ownership, and simplify management of investments.

Which Is Better?

The answer depends on the objective.

If the goal is retirement accumulation, tax advantages, and potentially passing retirement assets directly to heirs, a Solo 401(k) provides powerful benefits.

If the goal is long-term control, family wealth management, privacy, incapacity planning, and comprehensive estate planning, a trust may be more appropriate.

For many successful business owners, the strongest strategy is not choosing one over the other.

It is using both.

A properly structured Solo 401(k) can help build substantial retirement wealth while beneficiary designations may allow those assets to pass outside probate. At the same time, a trust can provide additional control, flexibility, and coordination for the rest of an individual's estate.

Final Thoughts

Estate planning is ultimately about more than avoiding taxes or court proceedings. It is about creating clarity, protecting loved ones, and ensuring that the wealth you worked hard to build is transferred according to your wishes.

A Solo 401(k) and a trust serve different purposes, but both can play valuable roles in a comprehensive estate plan. The Solo 401(k) provides a powerful platform for accumulating retirement wealth and potentially transferring those assets outside probate through beneficiary designations. A trust offers greater control, privacy, and long-term management capabilities that extend beyond retirement accounts.

For many entrepreneurs, investors, and self-employed professionals, combining these tools may provide the best opportunity to build wealth, protect assets, and create a lasting legacy for future generations.

This is not investment or legal tax advice; it is for educational purposes only. Consult a professional before making any legal or investment decisions.