by

Garrett Clark

Retirement Planning

What It Means to Be the Trustee of a Solo 401(k)

Learn what it means to be the trustee of a Solo 401(k), including the responsibilities, investment authority, checkbook control, compliance considerations, prohibited transaction rules, recordkeeping duties, and why understanding the trustee role is critical for self-directed retirement investing. This detailed guide from Survival401k explains how trustees oversee retirement plan assets while maintaining proper retirement plan administration and flexibility.

Search

Search

Category

Any Question?

Let’s talk

Any Question?

Let’s talk

Search

Search

Category

Any Question?

Let’s talk

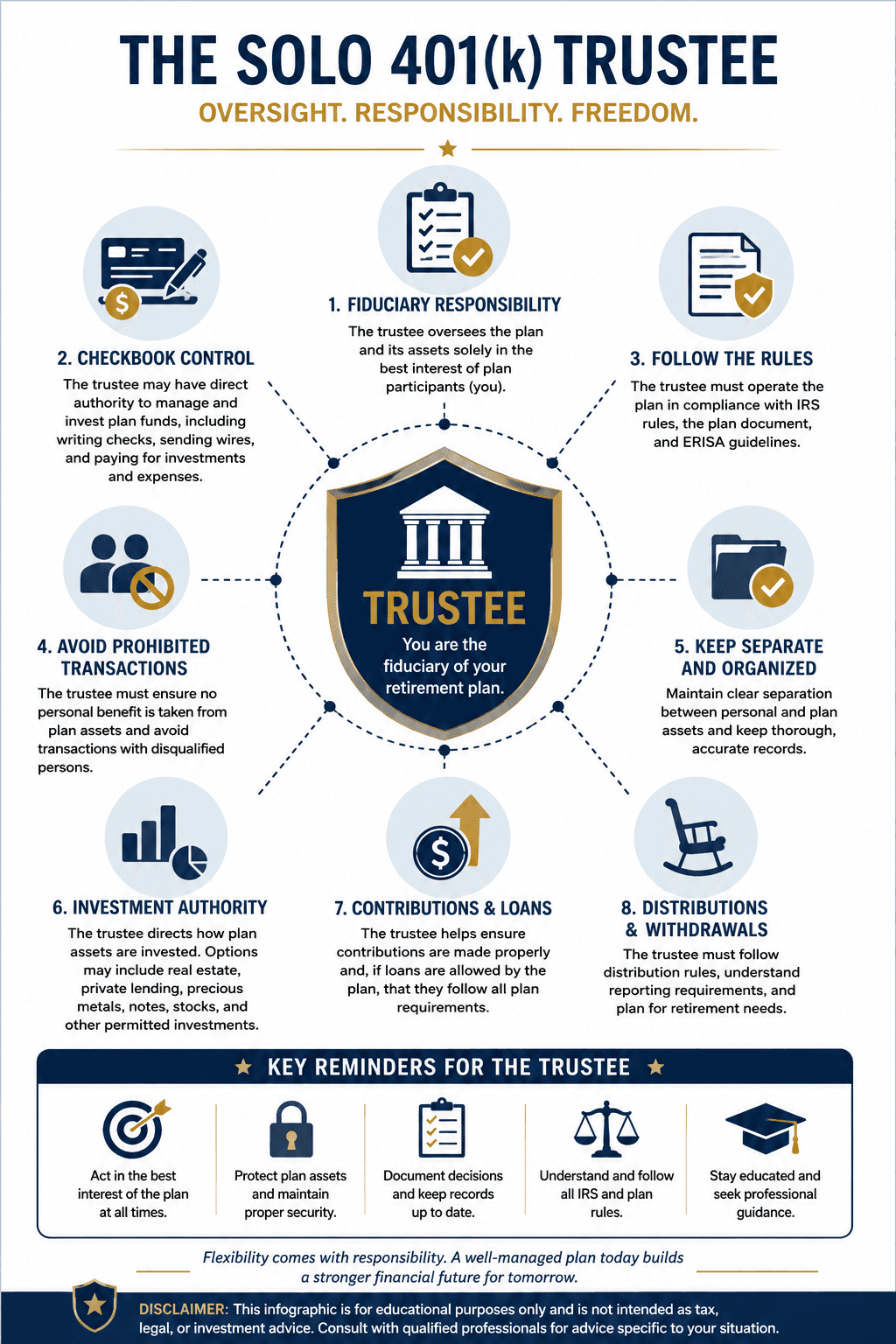

A Solo 401(k) can be one of the most powerful retirement planning tools available to self-employed individuals, business owners, freelancers, independent contractors, and side-hustle entrepreneurs. While many people focus on the contribution limits, tax strategies, or investment flexibility, one of the most important aspects of a Solo 401(k) is understanding the role of the plan trustee.

When you establish a Solo 401(k), you are not just opening another retirement account. In many cases, you are stepping into a position of responsibility and control over the retirement plan itself. The trustee plays a major role in how the plan is operated, how assets are managed, and how investments are handled.

At Survival401k, we believe education is critical to self-directed retirement planning. Understanding the responsibilities of being the trustee of your Solo 401(k) can help you make informed decisions and avoid costly mistakes.

What Is a Plan Trustee?

A trustee is the individual or entity responsible for overseeing and safeguarding the assets held in the retirement plan. In many Solo 401(k) structures, the business owner serves as the plan's trustee.

Unlike many traditional retirement accounts, where a financial institution controls the investments and account activity, a self-directed Solo 401(k) often allows the trustee to make investment decisions directly. This can provide significantly more flexibility, but it also comes with additional responsibility.

The trustee is essentially the person responsible for managing the plan according to the plan documents and applicable IRS regulations.

In simpler terms, the trustee is the individual tasked with helping ensure that the retirement plan is operated properly.

Why the Trustee Role Matters

The trustee role matters because the Solo 401(k) structure is designed to provide control and flexibility. With that flexibility comes responsibility.

In a standard brokerage retirement account, the institution may limit what investments are available and handle much of the administrative side. A self-directed Solo 401(k), however, may allow for investments outside of traditional Wall Street assets.

This can include investments such as:

Real estate

Precious metals

Private lending

Notes

Tax liens

Private placements

Certain alternative assets

Traditional investments like stocks, ETFs, and mutual funds

Because the trustee often has direct authority over the plan’s investment activity, the trustee must understand the rules and limitations associated with retirement accounts.

The trustee is not simply an investor. The trustee is overseeing retirement plan assets that must remain separate from personal assets and be handled according to retirement plan guidelines.

The Trustee Often Has Checkbook Control

One reason many investors pursue a Solo 401(k) is because of potential checkbook control.

Checkbook control generally refers to the ability for the trustee to directly authorize investments from the retirement account without needing approval from a third-party custodian for every transaction.

Depending on the structure of the plan, this may involve:

Opening a bank account in the name of the plan or related LLC

Writing checks directly from the retirement account structure

Sending wires for investments

Purchasing assets directly through the plan

Managing investment-related expenses from plan funds

This level of control can create speed and flexibility for investors who want to actively manage their retirement investments.

For example, a real estate investor may need to place earnest money quickly on a property opportunity. A private lender may need to fund a deal within a short timeframe. A precious metals investor may want direct purchasing authority.

In many cases, the trustee is the person facilitating these transactions on behalf of the retirement plan.

Being the Trustee Does Not Mean You Can Ignore the Rules

One of the biggest misconceptions about self-directed retirement plans is that greater control means fewer rules.

The opposite is often true.

The trustee must understand that retirement plans are still governed by IRS rules and regulations. The flexibility of a Solo 401(k) does not remove the responsibility to follow retirement plan requirements.

The trustee should understand areas such as:

Prohibited transactions

Disqualified persons

Proper titling of investments

Recordkeeping requirements

Contribution limits

Distribution rules

Loan provisions

Plan administration responsibilities

Reporting requirements

Failure to properly operate the plan could potentially create tax consequences or compliance issues.

This is why education and proper guidance are extremely important.

Understanding Prohibited Transactions

One of the most important responsibilities of the trustee is avoiding prohibited transactions.

A prohibited transaction generally involves improper use of retirement plan assets or improper interactions between the plan and certain related individuals.

Examples may include:

Personally using property owned by the retirement plan

Mixing personal and retirement funds

Buying or selling assets improperly between yourself and the plan

Using retirement funds for personal benefit

Certain transactions involving close family members or businesses you control

The trustee must help ensure that retirement assets are being used for investment purposes and not personal use.

For example, if a Solo 401(k) purchases an investment property, the trustee generally cannot personally live in the property or use it for personal vacations. The property is owned for the benefit of the retirement plan.

Understanding these rules is critical because prohibited transactions can carry serious consequences.

Separating Personal and Retirement Assets

Another major responsibility of the trustee is maintaining separation between personal finances and retirement plan assets.

This is one of the foundational principles of retirement plan compliance.

The trustee should generally avoid:

Paying personal expenses from the plan

Depositing personal funds into plan accounts improperly

Combining personal and retirement money

Using retirement-owned assets for personal benefit

Instead, the trustee should help maintain clear documentation and separation of activity.

For example:

Rental income from retirement-owned real estate should generally flow back to the retirement plan

Expenses related to retirement-owned investments should generally be paid from retirement funds

Investment accounts should generally be titled correctly in the name of the plan or related entity

Maintaining proper separation can help support compliance and organization.

A Solo 401(k) can be one of the most powerful retirement planning tools available to self-employed individuals, business owners, freelancers, independent contractors, and side-hustle entrepreneurs. While many people focus on the contribution limits, tax strategies, or investment flexibility, one of the most important aspects of a Solo 401(k) is understanding the role of the plan trustee.

When you establish a Solo 401(k), you are not just opening another retirement account. In many cases, you are stepping into a position of responsibility and control over the retirement plan itself. The trustee plays a major role in how the plan is operated, how assets are managed, and how investments are handled.

At Survival401k, we believe education is critical to self-directed retirement planning. Understanding the responsibilities of being the trustee of your Solo 401(k) can help you make informed decisions and avoid costly mistakes.

What Is a Plan Trustee?

A trustee is the individual or entity responsible for overseeing and safeguarding the assets held in the retirement plan. In many Solo 401(k) structures, the business owner serves as the plan's trustee.

Unlike many traditional retirement accounts, where a financial institution controls the investments and account activity, a self-directed Solo 401(k) often allows the trustee to make investment decisions directly. This can provide significantly more flexibility, but it also comes with additional responsibility.

The trustee is essentially the person responsible for managing the plan according to the plan documents and applicable IRS regulations.

In simpler terms, the trustee is the individual tasked with helping ensure that the retirement plan is operated properly.

Why the Trustee Role Matters

The trustee role matters because the Solo 401(k) structure is designed to provide control and flexibility. With that flexibility comes responsibility.

In a standard brokerage retirement account, the institution may limit what investments are available and handle much of the administrative side. A self-directed Solo 401(k), however, may allow for investments outside of traditional Wall Street assets.

This can include investments such as:

Real estate

Precious metals

Private lending

Notes

Tax liens

Private placements

Certain alternative assets

Traditional investments like stocks, ETFs, and mutual funds

Because the trustee often has direct authority over the plan’s investment activity, the trustee must understand the rules and limitations associated with retirement accounts.

The trustee is not simply an investor. The trustee is overseeing retirement plan assets that must remain separate from personal assets and be handled according to retirement plan guidelines.

The Trustee Often Has Checkbook Control

One reason many investors pursue a Solo 401(k) is because of potential checkbook control.

Checkbook control generally refers to the ability for the trustee to directly authorize investments from the retirement account without needing approval from a third-party custodian for every transaction.

Depending on the structure of the plan, this may involve:

Opening a bank account in the name of the plan or related LLC

Writing checks directly from the retirement account structure

Sending wires for investments

Purchasing assets directly through the plan

Managing investment-related expenses from plan funds

This level of control can create speed and flexibility for investors who want to actively manage their retirement investments.

For example, a real estate investor may need to place earnest money quickly on a property opportunity. A private lender may need to fund a deal within a short timeframe. A precious metals investor may want direct purchasing authority.

In many cases, the trustee is the person facilitating these transactions on behalf of the retirement plan.

Being the Trustee Does Not Mean You Can Ignore the Rules

One of the biggest misconceptions about self-directed retirement plans is that greater control means fewer rules.

The opposite is often true.

The trustee must understand that retirement plans are still governed by IRS rules and regulations. The flexibility of a Solo 401(k) does not remove the responsibility to follow retirement plan requirements.

The trustee should understand areas such as:

Prohibited transactions

Disqualified persons

Proper titling of investments

Recordkeeping requirements

Contribution limits

Distribution rules

Loan provisions

Plan administration responsibilities

Reporting requirements

Failure to properly operate the plan could potentially create tax consequences or compliance issues.

This is why education and proper guidance are extremely important.

Understanding Prohibited Transactions

One of the most important responsibilities of the trustee is avoiding prohibited transactions.

A prohibited transaction generally involves improper use of retirement plan assets or improper interactions between the plan and certain related individuals.

Examples may include:

Personally using property owned by the retirement plan

Mixing personal and retirement funds

Buying or selling assets improperly between yourself and the plan

Using retirement funds for personal benefit

Certain transactions involving close family members or businesses you control

The trustee must help ensure that retirement assets are being used for investment purposes and not personal use.

For example, if a Solo 401(k) purchases an investment property, the trustee generally cannot personally live in the property or use it for personal vacations. The property is owned for the benefit of the retirement plan.

Understanding these rules is critical because prohibited transactions can carry serious consequences.

Separating Personal and Retirement Assets

Another major responsibility of the trustee is maintaining separation between personal finances and retirement plan assets.

This is one of the foundational principles of retirement plan compliance.

The trustee should generally avoid:

Paying personal expenses from the plan

Depositing personal funds into plan accounts improperly

Combining personal and retirement money

Using retirement-owned assets for personal benefit

Instead, the trustee should help maintain clear documentation and separation of activity.

For example:

Rental income from retirement-owned real estate should generally flow back to the retirement plan

Expenses related to retirement-owned investments should generally be paid from retirement funds

Investment accounts should generally be titled correctly in the name of the plan or related entity

Maintaining proper separation can help support compliance and organization.

The Trustee and Investment Decisions

In many self-directed Solo 401(k) plans, the trustee has authority over investment decisions.

This can be empowering because it allows investors to diversify beyond traditional market investments if permitted under the plan.

Some individuals use Solo 401(k)s to invest in:

Rental properties

Short-term lending

Precious metals

Syndications

Startups

Land

Equipment

Cryptocurrency-related investments

Private notes

Others prefer more traditional investing through stocks, bonds, ETFs, and mutual funds.

The trustee is responsible for evaluating opportunities and making decisions on behalf of the retirement plan.

This does not necessarily mean every investment will be successful. Like any investment account, risk still exists.

However, many investors value the ability to make decisions directly instead of relying solely on standard brokerage investment menus.

Recordkeeping Responsibilities

Being the trustee also means maintaining proper records related to the retirement plan.

Good documentation can be extremely important for an organization, tax reporting, and demonstrating compliance.

Examples of records the trustee may want to maintain include:

Bank statements

Investment purchase documents

Wire confirmations

Contribution records

Expense receipts

Property records

Loan documentation

Precious metals invoices

Plan-related agreements

Annual valuations when applicable

Keeping organized records may help simplify future reporting and administration requirements.

The Trustee and Plan Contributions

The trustee may also play a role in ensuring contributions are handled properly.

Solo 401(k) plans can potentially allow both employee and employer contributions, depending on eligibility and business income.

Contribution limits can change over time based on IRS guidelines. The trustee should generally understand:

Contribution deadlines

Contribution calculations

Catch-up contributions when applicable

Roth contribution options, if available under the plan

Employer contribution structures

Improper contributions may create correction requirements or tax complications.

Understanding Distributions and Withdrawals

The trustee should also understand how distributions work.

A retirement plan is designed for retirement purposes, and withdrawals are generally governed by IRS distribution rules.

The trustee may need to understand:

Early withdrawal considerations

Required reporting forms

Roth distribution rules

Rollovers

In-service distribution rules, if applicable

Required minimum distributions when applicable

When distributions occur, proper reporting may be required depending on the situation.

The Trustee and Solo 401(k) Loans

Some Solo 401(k) plans may allow participant loans if permitted under the plan documents.

This is another feature that attracts many investors to the Solo 401(k) structure.

The trustee may be responsible for helping ensure:

Loans follow plan rules

Loan limits are observed

Repayment schedules are maintained

Documentation is retained

Payments are handled properly

Like all retirement plan features, loans must generally follow applicable guidelines.

Working With Professionals

Even though the trustee may have significant authority and control, that does not mean they must operate entirely alone.

Many trustees work with professionals such as:

CPAs

Tax professionals

Attorneys

Retirement plan providers

Financial professionals

Title companies

Banks

Real estate professionals

At Survival401k, education is a major focus because understanding the structure and responsibilities of the plan is extremely important.

A properly structured and properly operated Solo 401(k) can become a long-term financial tool for many investors and business owners.

Why Many Investors Value the Trustee Role

Many self-employed individuals pursue Solo 401(k)s because they want greater control over their retirement strategy.

Instead of being limited to traditional investment options, they may want the ability to actively direct retirement funds into opportunities they understand best.

For some people, that means real estate.

For others, it may mean private lending, precious metals, small business investing, or alternative assets.

The trustee role gives the investor a more active position in managing retirement wealth.

For disciplined and educated investors, this flexibility can be extremely valuable.

Final Thoughts

Being the trustee of a Solo 401(k) is about more than simply having access to retirement funds. It involves responsibility, organization, compliance awareness, and active oversight of the retirement plan.

The trustee role can provide significant flexibility and control, but it also requires understanding how retirement plans are meant to operate.

For many entrepreneurs, investors, freelancers, and business owners, the ability to direct retirement investments personally is one of the biggest advantages of a self-directed Solo 401(k).

However, with that opportunity comes the importance of education and proper administration.

At Survival401k, our goal is to help educate individuals on the potential benefits, responsibilities, and structures associated with self-directed Solo 401(k) plans so they can make informed decisions about their financial future.

This article is for educational purposes only and should not be considered tax, legal, or investment advice.

The Trustee and Investment Decisions

In many self-directed Solo 401(k) plans, the trustee has authority over investment decisions.

This can be empowering because it allows investors to diversify beyond traditional market investments if permitted under the plan.

Some individuals use Solo 401(k)s to invest in:

Rental properties

Short-term lending

Precious metals

Syndications

Startups

Land

Equipment

Cryptocurrency-related investments

Private notes

Others prefer more traditional investing through stocks, bonds, ETFs, and mutual funds.

The trustee is responsible for evaluating opportunities and making decisions on behalf of the retirement plan.

This does not necessarily mean every investment will be successful. Like any investment account, risk still exists.

However, many investors value the ability to make decisions directly instead of relying solely on standard brokerage investment menus.

Recordkeeping Responsibilities

Being the trustee also means maintaining proper records related to the retirement plan.

Good documentation can be extremely important for an organization, tax reporting, and demonstrating compliance.

Examples of records the trustee may want to maintain include:

Bank statements

Investment purchase documents

Wire confirmations

Contribution records

Expense receipts

Property records

Loan documentation

Precious metals invoices

Plan-related agreements

Annual valuations when applicable

Keeping organized records may help simplify future reporting and administration requirements.

The Trustee and Plan Contributions

The trustee may also play a role in ensuring contributions are handled properly.

Solo 401(k) plans can potentially allow both employee and employer contributions, depending on eligibility and business income.

Contribution limits can change over time based on IRS guidelines. The trustee should generally understand:

Contribution deadlines

Contribution calculations

Catch-up contributions when applicable

Roth contribution options, if available under the plan

Employer contribution structures

Improper contributions may create correction requirements or tax complications.

Understanding Distributions and Withdrawals

The trustee should also understand how distributions work.

A retirement plan is designed for retirement purposes, and withdrawals are generally governed by IRS distribution rules.

The trustee may need to understand:

Early withdrawal considerations

Required reporting forms

Roth distribution rules

Rollovers

In-service distribution rules, if applicable

Required minimum distributions when applicable

When distributions occur, proper reporting may be required depending on the situation.

The Trustee and Solo 401(k) Loans

Some Solo 401(k) plans may allow participant loans if permitted under the plan documents.

This is another feature that attracts many investors to the Solo 401(k) structure.

The trustee may be responsible for helping ensure:

Loans follow plan rules

Loan limits are observed

Repayment schedules are maintained

Documentation is retained

Payments are handled properly

Like all retirement plan features, loans must generally follow applicable guidelines.

Working With Professionals

Even though the trustee may have significant authority and control, that does not mean they must operate entirely alone.

Many trustees work with professionals such as:

CPAs

Tax professionals

Attorneys

Retirement plan providers

Financial professionals

Title companies

Banks

Real estate professionals

At Survival401k, education is a major focus because understanding the structure and responsibilities of the plan is extremely important.

A properly structured and properly operated Solo 401(k) can become a long-term financial tool for many investors and business owners.

Why Many Investors Value the Trustee Role

Many self-employed individuals pursue Solo 401(k)s because they want greater control over their retirement strategy.

Instead of being limited to traditional investment options, they may want the ability to actively direct retirement funds into opportunities they understand best.

For some people, that means real estate.

For others, it may mean private lending, precious metals, small business investing, or alternative assets.

The trustee role gives the investor a more active position in managing retirement wealth.

For disciplined and educated investors, this flexibility can be extremely valuable.

Final Thoughts

Being the trustee of a Solo 401(k) is about more than simply having access to retirement funds. It involves responsibility, organization, compliance awareness, and active oversight of the retirement plan.

The trustee role can provide significant flexibility and control, but it also requires understanding how retirement plans are meant to operate.

For many entrepreneurs, investors, freelancers, and business owners, the ability to direct retirement investments personally is one of the biggest advantages of a self-directed Solo 401(k).

However, with that opportunity comes the importance of education and proper administration.

At Survival401k, our goal is to help educate individuals on the potential benefits, responsibilities, and structures associated with self-directed Solo 401(k) plans so they can make informed decisions about their financial future.

This article is for educational purposes only and should not be considered tax, legal, or investment advice.

A Solo 401(k) can be one of the most powerful retirement planning tools available to self-employed individuals, business owners, freelancers, independent contractors, and side-hustle entrepreneurs. While many people focus on the contribution limits, tax strategies, or investment flexibility, one of the most important aspects of a Solo 401(k) is understanding the role of the plan trustee.

When you establish a Solo 401(k), you are not just opening another retirement account. In many cases, you are stepping into a position of responsibility and control over the retirement plan itself. The trustee plays a major role in how the plan is operated, how assets are managed, and how investments are handled.

At Survival401k, we believe education is critical to self-directed retirement planning. Understanding the responsibilities of being the trustee of your Solo 401(k) can help you make informed decisions and avoid costly mistakes.

What Is a Plan Trustee?

A trustee is the individual or entity responsible for overseeing and safeguarding the assets held in the retirement plan. In many Solo 401(k) structures, the business owner serves as the plan's trustee.

Unlike many traditional retirement accounts, where a financial institution controls the investments and account activity, a self-directed Solo 401(k) often allows the trustee to make investment decisions directly. This can provide significantly more flexibility, but it also comes with additional responsibility.

The trustee is essentially the person responsible for managing the plan according to the plan documents and applicable IRS regulations.

In simpler terms, the trustee is the individual tasked with helping ensure that the retirement plan is operated properly.

Why the Trustee Role Matters

The trustee role matters because the Solo 401(k) structure is designed to provide control and flexibility. With that flexibility comes responsibility.

In a standard brokerage retirement account, the institution may limit what investments are available and handle much of the administrative side. A self-directed Solo 401(k), however, may allow for investments outside of traditional Wall Street assets.

This can include investments such as:

Real estate

Precious metals

Private lending

Notes

Tax liens

Private placements

Certain alternative assets

Traditional investments like stocks, ETFs, and mutual funds

Because the trustee often has direct authority over the plan’s investment activity, the trustee must understand the rules and limitations associated with retirement accounts.

The trustee is not simply an investor. The trustee is overseeing retirement plan assets that must remain separate from personal assets and be handled according to retirement plan guidelines.

The Trustee Often Has Checkbook Control

One reason many investors pursue a Solo 401(k) is because of potential checkbook control.

Checkbook control generally refers to the ability for the trustee to directly authorize investments from the retirement account without needing approval from a third-party custodian for every transaction.

Depending on the structure of the plan, this may involve:

Opening a bank account in the name of the plan or related LLC

Writing checks directly from the retirement account structure

Sending wires for investments

Purchasing assets directly through the plan

Managing investment-related expenses from plan funds

This level of control can create speed and flexibility for investors who want to actively manage their retirement investments.

For example, a real estate investor may need to place earnest money quickly on a property opportunity. A private lender may need to fund a deal within a short timeframe. A precious metals investor may want direct purchasing authority.

In many cases, the trustee is the person facilitating these transactions on behalf of the retirement plan.

Being the Trustee Does Not Mean You Can Ignore the Rules

One of the biggest misconceptions about self-directed retirement plans is that greater control means fewer rules.

The opposite is often true.

The trustee must understand that retirement plans are still governed by IRS rules and regulations. The flexibility of a Solo 401(k) does not remove the responsibility to follow retirement plan requirements.

The trustee should understand areas such as:

Prohibited transactions

Disqualified persons

Proper titling of investments

Recordkeeping requirements

Contribution limits

Distribution rules

Loan provisions

Plan administration responsibilities

Reporting requirements

Failure to properly operate the plan could potentially create tax consequences or compliance issues.

This is why education and proper guidance are extremely important.

Understanding Prohibited Transactions

One of the most important responsibilities of the trustee is avoiding prohibited transactions.

A prohibited transaction generally involves improper use of retirement plan assets or improper interactions between the plan and certain related individuals.

Examples may include:

Personally using property owned by the retirement plan

Mixing personal and retirement funds

Buying or selling assets improperly between yourself and the plan

Using retirement funds for personal benefit

Certain transactions involving close family members or businesses you control

The trustee must help ensure that retirement assets are being used for investment purposes and not personal use.

For example, if a Solo 401(k) purchases an investment property, the trustee generally cannot personally live in the property or use it for personal vacations. The property is owned for the benefit of the retirement plan.

Understanding these rules is critical because prohibited transactions can carry serious consequences.

Separating Personal and Retirement Assets

Another major responsibility of the trustee is maintaining separation between personal finances and retirement plan assets.

This is one of the foundational principles of retirement plan compliance.

The trustee should generally avoid:

Paying personal expenses from the plan

Depositing personal funds into plan accounts improperly

Combining personal and retirement money

Using retirement-owned assets for personal benefit

Instead, the trustee should help maintain clear documentation and separation of activity.

For example:

Rental income from retirement-owned real estate should generally flow back to the retirement plan

Expenses related to retirement-owned investments should generally be paid from retirement funds

Investment accounts should generally be titled correctly in the name of the plan or related entity

Maintaining proper separation can help support compliance and organization.

The Trustee and Investment Decisions

In many self-directed Solo 401(k) plans, the trustee has authority over investment decisions.

This can be empowering because it allows investors to diversify beyond traditional market investments if permitted under the plan.

Some individuals use Solo 401(k)s to invest in:

Rental properties

Short-term lending

Precious metals

Syndications

Startups

Land

Equipment

Cryptocurrency-related investments

Private notes

Others prefer more traditional investing through stocks, bonds, ETFs, and mutual funds.

The trustee is responsible for evaluating opportunities and making decisions on behalf of the retirement plan.

This does not necessarily mean every investment will be successful. Like any investment account, risk still exists.

However, many investors value the ability to make decisions directly instead of relying solely on standard brokerage investment menus.

Recordkeeping Responsibilities

Being the trustee also means maintaining proper records related to the retirement plan.

Good documentation can be extremely important for an organization, tax reporting, and demonstrating compliance.

Examples of records the trustee may want to maintain include:

Bank statements

Investment purchase documents

Wire confirmations

Contribution records

Expense receipts

Property records

Loan documentation

Precious metals invoices

Plan-related agreements

Annual valuations when applicable

Keeping organized records may help simplify future reporting and administration requirements.

The Trustee and Plan Contributions

The trustee may also play a role in ensuring contributions are handled properly.

Solo 401(k) plans can potentially allow both employee and employer contributions, depending on eligibility and business income.

Contribution limits can change over time based on IRS guidelines. The trustee should generally understand:

Contribution deadlines

Contribution calculations

Catch-up contributions when applicable

Roth contribution options, if available under the plan

Employer contribution structures

Improper contributions may create correction requirements or tax complications.

Understanding Distributions and Withdrawals

The trustee should also understand how distributions work.

A retirement plan is designed for retirement purposes, and withdrawals are generally governed by IRS distribution rules.

The trustee may need to understand:

Early withdrawal considerations

Required reporting forms

Roth distribution rules

Rollovers

In-service distribution rules, if applicable

Required minimum distributions when applicable

When distributions occur, proper reporting may be required depending on the situation.

The Trustee and Solo 401(k) Loans

Some Solo 401(k) plans may allow participant loans if permitted under the plan documents.

This is another feature that attracts many investors to the Solo 401(k) structure.

The trustee may be responsible for helping ensure:

Loans follow plan rules

Loan limits are observed

Repayment schedules are maintained

Documentation is retained

Payments are handled properly

Like all retirement plan features, loans must generally follow applicable guidelines.

Working With Professionals

Even though the trustee may have significant authority and control, that does not mean they must operate entirely alone.

Many trustees work with professionals such as:

CPAs

Tax professionals

Attorneys

Retirement plan providers

Financial professionals

Title companies

Banks

Real estate professionals

At Survival401k, education is a major focus because understanding the structure and responsibilities of the plan is extremely important.

A properly structured and properly operated Solo 401(k) can become a long-term financial tool for many investors and business owners.

Why Many Investors Value the Trustee Role

Many self-employed individuals pursue Solo 401(k)s because they want greater control over their retirement strategy.

Instead of being limited to traditional investment options, they may want the ability to actively direct retirement funds into opportunities they understand best.

For some people, that means real estate.

For others, it may mean private lending, precious metals, small business investing, or alternative assets.

The trustee role gives the investor a more active position in managing retirement wealth.

For disciplined and educated investors, this flexibility can be extremely valuable.

Final Thoughts

Being the trustee of a Solo 401(k) is about more than simply having access to retirement funds. It involves responsibility, organization, compliance awareness, and active oversight of the retirement plan.

The trustee role can provide significant flexibility and control, but it also requires understanding how retirement plans are meant to operate.

For many entrepreneurs, investors, freelancers, and business owners, the ability to direct retirement investments personally is one of the biggest advantages of a self-directed Solo 401(k).

However, with that opportunity comes the importance of education and proper administration.

At Survival401k, our goal is to help educate individuals on the potential benefits, responsibilities, and structures associated with self-directed Solo 401(k) plans so they can make informed decisions about their financial future.

This article is for educational purposes only and should not be considered tax, legal, or investment advice.