by

Garrett Clark

Tax Planning

How Entrepreneurs Can Potentially Shelter More Income

Learn how entrepreneurs and self-employed business owners may potentially shelter more income through legal, tax-advantaged retirement strategies like the Solo 401(k). Explore contribution opportunities, tax-deferred growth, investment flexibility, and important rules every business owner should understand when building long-term wealth.

Search

Search

Category

Any Question?

Let’s talk

Any Question?

Let’s talk

Search

Search

Category

Any Question?

Let’s talk

Understanding Tax-Advantaged Retirement Strategies for Business Owners

Entrepreneurs, business owners, freelancers, independent contractors, and self-employed professionals often spend years focused on growing income, building businesses, hiring teams, and increasing revenue. However, one area many overlook is how to potentially protect and position more of that income for long-term wealth building.

For many entrepreneurs, taxes become one of the single largest expenses they face as income grows. While taxes are a normal part of business, there are legal and IRS-recognized strategies that may help eligible business owners potentially reduce taxable income while simultaneously building retirement savings.

One of the most powerful tools many self-employed individuals explore is the Solo 401(k).

Why Entrepreneurs Often Face Higher Tax Pressure

Unlike traditional employees who may rely heavily on employer retirement plans, entrepreneurs often:

Generate variable income

Pay self-employment taxes

Have fewer automatic retirement systems

Need to create their own long-term investment strategy

Carry greater responsibility for tax planning

As businesses grow, many entrepreneurs discover that simply earning more money does not automatically create more wealth if a significant portion continually leaves through taxes and unnecessary spending.

This is why many business owners begin looking into:

Retirement contribution strategies

Tax-advantaged investing

Business deductions

Long-term asset accumulation

Alternative investment opportunities

What Is “Sheltering Income”?

The phrase “sheltering income” does not mean hiding money or avoiding taxes illegally.

Instead, it generally refers to using legal, IRS-approved structures that may allow you to:

Potentially reduce current taxable income

Delay taxation until retirement

Build investments in tax-advantaged accounts

Position money for long-term compounding

Create separation between personal spending and retirement investing

For eligible entrepreneurs, retirement accounts can become one of the primary ways to potentially accomplish this.

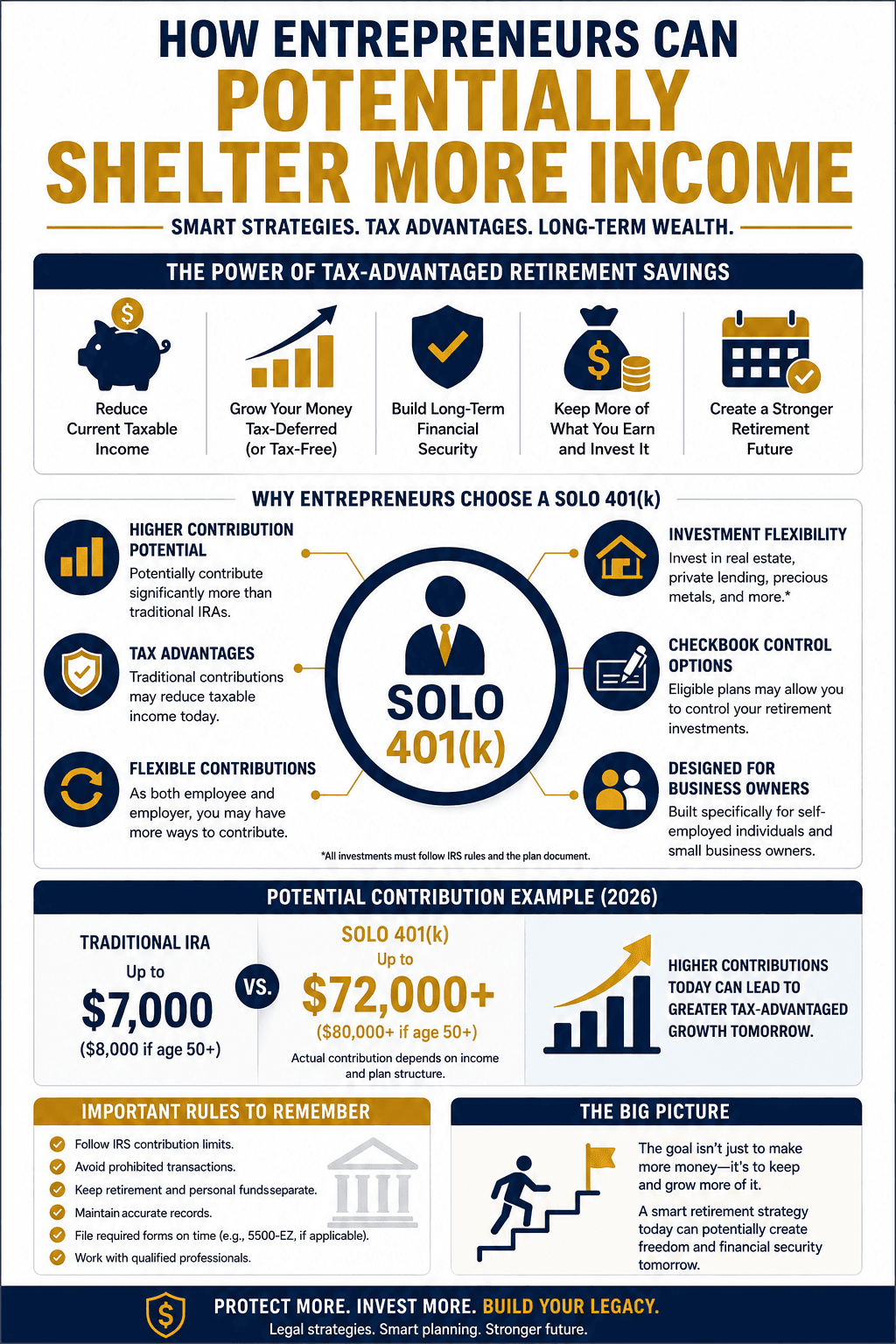

Why Many Entrepreneurs Explore the Solo 401(k)

A Solo 401(k), sometimes called an Individual 401(k), is a retirement plan designed for self-employed individuals or business owners with no full-time employees other than a spouse.

Many entrepreneurs explore Solo 401(k)s because they may offer:

High contribution limits

Traditional and Roth contribution options

Potential tax deductions

Flexible investment options

Possible checkbook-control structures

The ability to invest beyond traditional Wall Street assets

For business owners trying to potentially shelter more income while still investing for the future, this structure can become extremely attractive.

Higher Contribution Potential

One reason entrepreneurs often favor Solo 401(k)s is the potentially higher contribution limits compared to many other retirement accounts.

Depending on income, age, and business structure, eligible individuals may potentially contribute significantly more than they could through a traditional IRA.

This can allow:

More money to potentially grow tax-deferred

Larger deductions in certain situations

Greater long-term compounding opportunities

More aggressive retirement savings strategies

For high-income entrepreneurs, this can become an important component of overall financial planning.

Traditional vs Roth Contributions

Many Solo 401(k) plans may offer both:

Traditional contributions

Roth contributions

Traditional Contributions

Traditional contributions are generally made pre-tax, which may reduce taxable income in the current year.

This is often the area entrepreneurs focus on when discussing potential income sheltering strategies.

Potential advantages may include:

Lower current taxable income

Deferred taxation until distribution

More investable capital remaining inside the account

Roth Contributions

Roth contributions are made after taxes but may allow for tax-free qualified withdrawals later under current tax law.

Some entrepreneurs choose a combination strategy depending on:

Current income

Future tax expectations

Business growth projections

Retirement goals

The Potential Power of Tax-Deferred Growth

One major advantage of retirement accounts is compounding.

When money remains invested inside a tax-advantaged structure, gains may continue compounding over time without annual taxation in many situations.

Over long periods, this may potentially create significant differences compared to fully taxable investing environments.

Entrepreneurs often understand the value of reinvesting capital into business growth. Retirement accounts can operate similarly by allowing eligible investments to potentially continue growing within the account structure.

Business Owners Often Have More Flexibility

Entrepreneurs sometimes have planning opportunities that traditional employees do not.

Business owners may potentially:

Adjust compensation strategies

Time contributions differently

Use multiple retirement strategies together

Structure businesses strategically

Create additional earned income streams

This flexibility is one reason many entrepreneurs work closely with:

CPAs

Tax professionals

Financial advisors

ERISA professionals

Retirement plan specialists

Important Rules and Responsibilities

While Solo 401(k)s can be powerful, they also come with responsibilities.

Business owners must understand:

Contribution limits

Filing requirements

Prohibited transaction rules

Disqualified person rules

Distribution rules

Recordkeeping requirements

Potential Form 5500-EZ obligations

Compliance responsibilities

Improper transactions or misuse of retirement funds can create serious tax consequences.

This is why education and proper plan administration are extremely important.

Common Mistakes Entrepreneurs Should Avoid

Mixing Personal and Retirement Funds

Retirement assets should generally remain separate from personal finances.

Ignoring Contribution Deadlines

Missing deadlines may reduce contribution opportunities.

Misunderstanding Prohibited Transactions

Certain transactions involving yourself, close family members, or controlled businesses may violate IRS rules.

Failing to Maintain Records

Documentation and compliance remain critical for retirement plans.

Assuming Every Investment Is Allowed

Even self-directed accounts still operate under IRS and plan rules.

Entrepreneurs Often Think Differently About Wealth

Many entrepreneurs naturally think beyond traditional investing.

They may value:

Control

Flexibility

Alternative investments

Business ownership

Real estate

Cash flow

Long-term asset growth

For some, self-directed retirement strategies align more closely with how they already think about investing and wealth building.

Final Thoughts

Entrepreneurs spend years building businesses, solving problems, taking risks, and creating income opportunities. However, protecting and positioning income effectively can become just as important as generating it.

For eligible business owners, retirement strategies like the Solo 401(k) may potentially provide:

Higher contribution opportunities

Tax-advantaged growth

Flexible investing options

Greater control

Long-term wealth-building potential

Every situation is different, and retirement planning should always be evaluated carefully with qualified professionals. However, for many entrepreneurs, learning how to potentially shelter more income legally and strategically can become a major turning point in long-term financial planning.

Learn More

If you would like to learn more about self-directed Solo 401(k) strategies, contribution structures, or investment flexibility, visit:

This article is for educational and informational purposes only and should not be considered tax, legal, or investment advice. Always consult with qualified professionals regarding your specific situation.

The Potential Power of Tax-Deferred Growth

One major advantage of retirement accounts is compounding.

When money remains invested inside a tax-advantaged structure, gains may continue compounding over time without annual taxation in many situations.

Over long periods, this may potentially create significant differences compared to fully taxable investing environments.

Entrepreneurs often understand the value of reinvesting capital into business growth. Retirement accounts can operate similarly by allowing eligible investments to potentially continue growing within the account structure.

Business Owners Often Have More Flexibility

Entrepreneurs sometimes have planning opportunities that traditional employees do not.

Business owners may potentially:

Adjust compensation strategies

Time contributions differently

Use multiple retirement strategies together

Structure businesses strategically

Create additional earned income streams

This flexibility is one reason many entrepreneurs work closely with:

CPAs

Tax professionals

Financial advisors

ERISA professionals

Retirement plan specialists

Important Rules and Responsibilities

While Solo 401(k)s can be powerful, they also come with responsibilities.

Business owners must understand:

Contribution limits

Filing requirements

Prohibited transaction rules

Disqualified person rules

Distribution rules

Recordkeeping requirements

Potential Form 5500-EZ obligations

Compliance responsibilities

Improper transactions or misuse of retirement funds can create serious tax consequences.

This is why education and proper plan administration are extremely important.

Common Mistakes Entrepreneurs Should Avoid

Mixing Personal and Retirement Funds

Retirement assets should generally remain separate from personal finances.

Ignoring Contribution Deadlines

Missing deadlines may reduce contribution opportunities.

Misunderstanding Prohibited Transactions

Certain transactions involving yourself, close family members, or controlled businesses may violate IRS rules.

Failing to Maintain Records

Documentation and compliance remain critical for retirement plans.

Assuming Every Investment Is Allowed

Even self-directed accounts still operate under IRS and plan rules.

Entrepreneurs Often Think Differently About Wealth

Many entrepreneurs naturally think beyond traditional investing.

They may value:

Control

Flexibility

Alternative investments

Business ownership

Real estate

Cash flow

Long-term asset growth

For some, self-directed retirement strategies align more closely with how they already think about investing and wealth building.

Final Thoughts

Entrepreneurs spend years building businesses, solving problems, taking risks, and creating income opportunities. However, protecting and positioning income effectively can become just as important as generating it.

For eligible business owners, retirement strategies like the Solo 401(k) may potentially provide:

Higher contribution opportunities

Tax-advantaged growth

Flexible investing options

Greater control

Long-term wealth-building potential

Every situation is different, and retirement planning should always be evaluated carefully with qualified professionals. However, for many entrepreneurs, learning how to potentially shelter more income legally and strategically can become a major turning point in long-term financial planning.

Learn More

If you would like to learn more about self-directed Solo 401(k) strategies, contribution structures, or investment flexibility, visit:

This article is for educational and informational purposes only and should not be considered tax, legal, or investment advice. Always consult with qualified professionals regarding your specific situation.

Understanding Tax-Advantaged Retirement Strategies for Business Owners

Entrepreneurs, business owners, freelancers, independent contractors, and self-employed professionals often spend years focused on growing income, building businesses, hiring teams, and increasing revenue. However, one area many overlook is how to potentially protect and position more of that income for long-term wealth building.

For many entrepreneurs, taxes become one of the single largest expenses they face as income grows. While taxes are a normal part of business, there are legal and IRS-recognized strategies that may help eligible business owners potentially reduce taxable income while simultaneously building retirement savings.

One of the most powerful tools many self-employed individuals explore is the Solo 401(k).

Why Entrepreneurs Often Face Higher Tax Pressure

Unlike traditional employees who may rely heavily on employer retirement plans, entrepreneurs often:

Generate variable income

Pay self-employment taxes

Have fewer automatic retirement systems

Need to create their own long-term investment strategy

Carry greater responsibility for tax planning

As businesses grow, many entrepreneurs discover that simply earning more money does not automatically create more wealth if a significant portion continually leaves through taxes and unnecessary spending.

This is why many business owners begin looking into:

Retirement contribution strategies

Tax-advantaged investing

Business deductions

Long-term asset accumulation

Alternative investment opportunities

What Is “Sheltering Income”?

The phrase “sheltering income” does not mean hiding money or avoiding taxes illegally.

Instead, it generally refers to using legal, IRS-approved structures that may allow you to:

Potentially reduce current taxable income

Delay taxation until retirement

Build investments in tax-advantaged accounts

Position money for long-term compounding

Create separation between personal spending and retirement investing

For eligible entrepreneurs, retirement accounts can become one of the primary ways to potentially accomplish this.

Why Many Entrepreneurs Explore the Solo 401(k)

A Solo 401(k), sometimes called an Individual 401(k), is a retirement plan designed for self-employed individuals or business owners with no full-time employees other than a spouse.

Many entrepreneurs explore Solo 401(k)s because they may offer:

High contribution limits

Traditional and Roth contribution options

Potential tax deductions

Flexible investment options

Possible checkbook-control structures

The ability to invest beyond traditional Wall Street assets

For business owners trying to potentially shelter more income while still investing for the future, this structure can become extremely attractive.

Higher Contribution Potential

One reason entrepreneurs often favor Solo 401(k)s is the potentially higher contribution limits compared to many other retirement accounts.

Depending on income, age, and business structure, eligible individuals may potentially contribute significantly more than they could through a traditional IRA.

This can allow:

More money to potentially grow tax-deferred

Larger deductions in certain situations

Greater long-term compounding opportunities

More aggressive retirement savings strategies

For high-income entrepreneurs, this can become an important component of overall financial planning.

Traditional vs Roth Contributions

Many Solo 401(k) plans may offer both:

Traditional contributions

Roth contributions

Traditional Contributions

Traditional contributions are generally made pre-tax, which may reduce taxable income in the current year.

This is often the area entrepreneurs focus on when discussing potential income sheltering strategies.

Potential advantages may include:

Lower current taxable income

Deferred taxation until distribution

More investable capital remaining inside the account

Roth Contributions

Roth contributions are made after taxes but may allow for tax-free qualified withdrawals later under current tax law.

Some entrepreneurs choose a combination strategy depending on:

Current income

Future tax expectations

Business growth projections

Retirement goals

The Potential Power of Tax-Deferred Growth

One major advantage of retirement accounts is compounding.

When money remains invested inside a tax-advantaged structure, gains may continue compounding over time without annual taxation in many situations.

Over long periods, this may potentially create significant differences compared to fully taxable investing environments.

Entrepreneurs often understand the value of reinvesting capital into business growth. Retirement accounts can operate similarly by allowing eligible investments to potentially continue growing within the account structure.

Business Owners Often Have More Flexibility

Entrepreneurs sometimes have planning opportunities that traditional employees do not.

Business owners may potentially:

Adjust compensation strategies

Time contributions differently

Use multiple retirement strategies together

Structure businesses strategically

Create additional earned income streams

This flexibility is one reason many entrepreneurs work closely with:

CPAs

Tax professionals

Financial advisors

ERISA professionals

Retirement plan specialists

Important Rules and Responsibilities

While Solo 401(k)s can be powerful, they also come with responsibilities.

Business owners must understand:

Contribution limits

Filing requirements

Prohibited transaction rules

Disqualified person rules

Distribution rules

Recordkeeping requirements

Potential Form 5500-EZ obligations

Compliance responsibilities

Improper transactions or misuse of retirement funds can create serious tax consequences.

This is why education and proper plan administration are extremely important.

Common Mistakes Entrepreneurs Should Avoid

Mixing Personal and Retirement Funds

Retirement assets should generally remain separate from personal finances.

Ignoring Contribution Deadlines

Missing deadlines may reduce contribution opportunities.

Misunderstanding Prohibited Transactions

Certain transactions involving yourself, close family members, or controlled businesses may violate IRS rules.

Failing to Maintain Records

Documentation and compliance remain critical for retirement plans.

Assuming Every Investment Is Allowed

Even self-directed accounts still operate under IRS and plan rules.

Entrepreneurs Often Think Differently About Wealth

Many entrepreneurs naturally think beyond traditional investing.

They may value:

Control

Flexibility

Alternative investments

Business ownership

Real estate

Cash flow

Long-term asset growth

For some, self-directed retirement strategies align more closely with how they already think about investing and wealth building.

Final Thoughts

Entrepreneurs spend years building businesses, solving problems, taking risks, and creating income opportunities. However, protecting and positioning income effectively can become just as important as generating it.

For eligible business owners, retirement strategies like the Solo 401(k) may potentially provide:

Higher contribution opportunities

Tax-advantaged growth

Flexible investing options

Greater control

Long-term wealth-building potential

Every situation is different, and retirement planning should always be evaluated carefully with qualified professionals. However, for many entrepreneurs, learning how to potentially shelter more income legally and strategically can become a major turning point in long-term financial planning.

Learn More

If you would like to learn more about self-directed Solo 401(k) strategies, contribution structures, or investment flexibility, visit:

This article is for educational and informational purposes only and should not be considered tax, legal, or investment advice. Always consult with qualified professionals regarding your specific situation.