by

Garrett Clark

Retirement Planning

Why Many Investors Want Control Over Their Retirement Investments

Many investors are starting to question traditional retirement accounts and the lack of control they offer. This blog explores why having control over your investments matters, how it impacts long-term wealth, and what options are available for building a more personalized retirement strategy.

Search

Search

Category

Any Question?

Let’s talk

Any Question?

Let’s talk

Search

Search

Category

Any Question?

Let’s talk

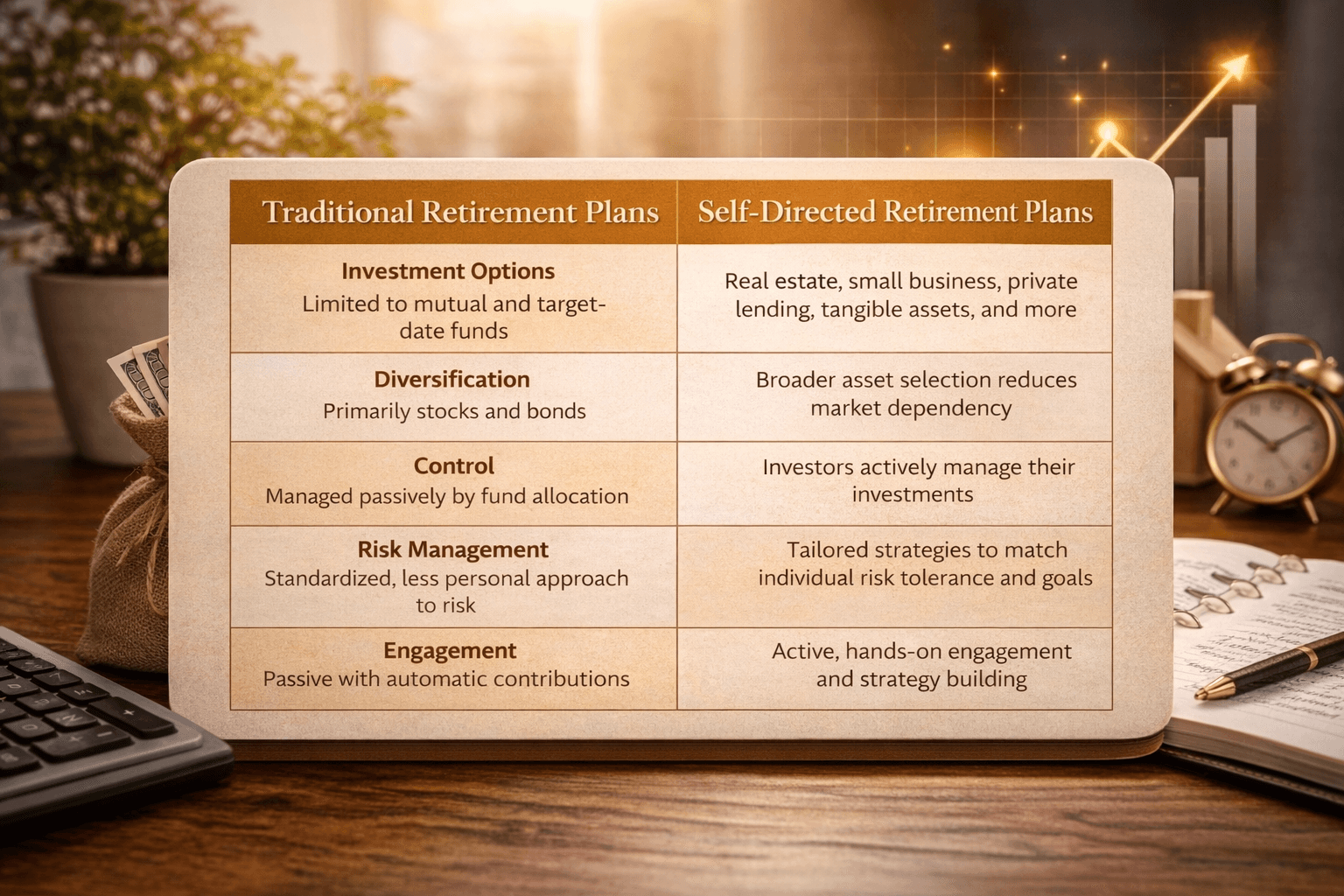

The Traditional Retirement Approach

For many people, retirement accounts are something they set up early in their career and rarely think about again. Contributions are made automatically, investments are selected from a limited list of options, and the account grows quietly in the background.

This system is designed for simplicity and consistency. For some investors, that’s enough.

But over time, many begin asking a deeper question:

Why don’t I have more control over my retirement investments?

As individuals grow in income, experience, and financial awareness, they often realize their retirement strategy hasn’t evolved with them.

Why the Desire for Control Increases

As investors become more financially educated, their expectations change. They begin to look beyond basic investment options and want strategies that align with their personal goals, knowledge, and long-term vision.

Instead of relying on pre-selected portfolios, they want the ability to:

Make intentional investment decisions

Allocate capital into areas they understand

Build strategies that reflect their financial goals

Control becomes less about complexity and more about alignment.

The Limitations of Traditional Plans

Employer-sponsored retirement plans often limit investors to a small selection of mutual funds or target-date funds. While these can be effective, they are designed for the average investor, not someone with specialized knowledge or experience.

This becomes a problem for individuals who:

Understand real estate investing

Have experience with private lending

Operate or invest in businesses

Want exposure to alternative assets

When these investors cannot allocate retirement funds into areas they understand, their strategy feels restricted.

Control Creates Strategic Flexibility

Having control over retirement investments allows individuals to design strategies that reflect their personal understanding of markets and opportunities.

For some, this means diversifying beyond public markets. For others, it means actively managing their portfolio instead of relying on default allocations.

This flexibility allows investors to:

Adjust strategies based on market conditions

Take advantage of opportunities they recognize

Align investments with their long-term vision

Instead of a one-size-fits-all approach, they create a system tailored to their situation.

Alignment With Real-World Experience

Many entrepreneurs and self-employed professionals build wealth through hands-on experience. They are used to evaluating risk, making decisions, and identifying opportunities.

When their retirement accounts don’t allow them to apply those same skills, it creates a disconnect.

Control bridges that gap.

It allows investors to apply the same strategic thinking they use in their businesses or personal investments to their retirement planning. This creates consistency across their financial life instead of treating retirement as a completely separate system.

Diversification Beyond the Stock Market

Traditional retirement accounts are heavily focused on stocks and bonds. While these are important, they are not the only investment options available.

Investors seeking more control often look to diversify into:

Real estate

Private credit or lending

Small business investments

Tangible assets

This broader approach allows them to build portfolios that are not solely dependent on public market performance.

Greater diversification can also help manage risk by spreading investments across multiple asset types.

Increased Engagement Leads to Better Outcomes

When investors have control, they tend to become more engaged with their financial planning.

Instead of viewing retirement as something passive, they begin to:

Monitor performance more closely

Adjust strategies over time

Make more intentional financial decisions

This level of involvement often leads to a deeper understanding of risk, timelines, and long-term planning.

It transforms retirement from a passive savings tool into an active wealth-building system.

“Control isn’t about doing more, it’s about aligning your investments with what you actually understand.”

Garrett Clark

Director of Sales

The Responsibility That Comes With Control

While control offers significant advantages, it also comes with responsibility.

Investors must understand:

The rules governing retirement accounts

Compliance requirements

Risks associated with different investments

Decisions should be made carefully and, when appropriate, with guidance from qualified professionals.

Having control does not eliminate risk. It simply gives you the ability to manage it more directly.

A Shift in How Investors Think

The growing demand for control reflects a larger shift in how people approach their finances.

Today’s investors are:

More informed

More entrepreneurial

More involved in decision-making

They are no longer satisfied with passive systems that operate in the background. Instead, they want strategies that reflect their knowledge, experience, and goals.

The New Approach to Retirement Planning

Retirement planning is no longer just about setting money aside and hoping it grows over time.

For many investors, it’s about building a system that:

Aligns with their income and lifestyle

Supports long-term wealth creation

Gives them flexibility and control

Having the ability to guide those investments themselves is becoming an essential part of modern financial planning.

Final Thoughts

Control over retirement investments is not about taking unnecessary risks or complicating your strategy.

It’s about creating alignment between your financial knowledge, your goals, and how your money is actually being used.

When done correctly, greater control allows investors to move from passive participation to active wealth building.

And that shift can make a significant difference over time.

This content is for educational purposes only and is not legal or tax advice. Please consult a qualified professional before making any financial or investment decisions.

The Traditional Retirement Approach

For many people, retirement accounts are something they set up early in their career and rarely think about again. Contributions are made automatically, investments are selected from a limited list of options, and the account grows quietly in the background.

This system is designed for simplicity and consistency. For some investors, that’s enough.

But over time, many begin asking a deeper question:

Why don’t I have more control over my retirement investments?

As individuals grow in income, experience, and financial awareness, they often realize their retirement strategy hasn’t evolved with them.

Why the Desire for Control Increases

As investors become more financially educated, their expectations change. They begin to look beyond basic investment options and want strategies that align with their personal goals, knowledge, and long-term vision.

Instead of relying on pre-selected portfolios, they want the ability to:

Make intentional investment decisions

Allocate capital into areas they understand

Build strategies that reflect their financial goals

Control becomes less about complexity and more about alignment.

The Limitations of Traditional Plans

Employer-sponsored retirement plans often limit investors to a small selection of mutual funds or target-date funds. While these can be effective, they are designed for the average investor, not someone with specialized knowledge or experience.

This becomes a problem for individuals who:

Understand real estate investing

Have experience with private lending

Operate or invest in businesses

Want exposure to alternative assets

When these investors cannot allocate retirement funds into areas they understand, their strategy feels restricted.

Control Creates Strategic Flexibility

Having control over retirement investments allows individuals to design strategies that reflect their personal understanding of markets and opportunities.

For some, this means diversifying beyond public markets. For others, it means actively managing their portfolio instead of relying on default allocations.

This flexibility allows investors to:

Adjust strategies based on market conditions

Take advantage of opportunities they recognize

Align investments with their long-term vision

Instead of a one-size-fits-all approach, they create a system tailored to their situation.

Alignment With Real-World Experience

Many entrepreneurs and self-employed professionals build wealth through hands-on experience. They are used to evaluating risk, making decisions, and identifying opportunities.

When their retirement accounts don’t allow them to apply those same skills, it creates a disconnect.

Control bridges that gap.

It allows investors to apply the same strategic thinking they use in their businesses or personal investments to their retirement planning. This creates consistency across their financial life instead of treating retirement as a completely separate system.

Diversification Beyond the Stock Market

Traditional retirement accounts are heavily focused on stocks and bonds. While these are important, they are not the only investment options available.

Investors seeking more control often look to diversify into:

Real estate

Private credit or lending

Small business investments

Tangible assets

This broader approach allows them to build portfolios that are not solely dependent on public market performance.

Greater diversification can also help manage risk by spreading investments across multiple asset types.

Increased Engagement Leads to Better Outcomes

When investors have control, they tend to become more engaged with their financial planning.

Instead of viewing retirement as something passive, they begin to:

Monitor performance more closely

Adjust strategies over time

Make more intentional financial decisions

This level of involvement often leads to a deeper understanding of risk, timelines, and long-term planning.

It transforms retirement from a passive savings tool into an active wealth-building system.

“Control isn’t about doing more, it’s about aligning your investments with what you actually understand.”

Garrett Clark

Director of Sales

The Responsibility That Comes With Control

While control offers significant advantages, it also comes with responsibility.

Investors must understand:

The rules governing retirement accounts

Compliance requirements

Risks associated with different investments

Decisions should be made carefully and, when appropriate, with guidance from qualified professionals.

Having control does not eliminate risk. It simply gives you the ability to manage it more directly.

A Shift in How Investors Think

The growing demand for control reflects a larger shift in how people approach their finances.

Today’s investors are:

More informed

More entrepreneurial

More involved in decision-making

They are no longer satisfied with passive systems that operate in the background. Instead, they want strategies that reflect their knowledge, experience, and goals.

The New Approach to Retirement Planning

Retirement planning is no longer just about setting money aside and hoping it grows over time.

For many investors, it’s about building a system that:

Aligns with their income and lifestyle

Supports long-term wealth creation

Gives them flexibility and control

Having the ability to guide those investments themselves is becoming an essential part of modern financial planning.

Final Thoughts

Control over retirement investments is not about taking unnecessary risks or complicating your strategy.

It’s about creating alignment between your financial knowledge, your goals, and how your money is actually being used.

When done correctly, greater control allows investors to move from passive participation to active wealth building.

And that shift can make a significant difference over time.

This content is for educational purposes only and is not legal or tax advice. Please consult a qualified professional before making any financial or investment decisions.